Ever added something to your cart, saw the total… and immediately started doing mental math?

You’re not alone. BNPL market value reached a staggering $107 billion in 2025—and for good reason. Apps like Afterpay can help you split a single, larger bill into four smaller ones spread out over time, so you can focus on your cash flow.

However, Afterpay may not be the right fit for everyone.

If you’re looking for other options, you’re in the right place. Below, I’m keeping it quick and useful, with a short take on each app, plus a fact sheet to help you compare and find your perfect match. Let’s get started.

Key Takeaways

- Pick A Plan That Fits: Apps like Afterpay offer different payment setups, so choose one that matches your budget and repayment timeline.

- Watch Fees And Interest: Look for BNPL apps that clearly explain interest rates and fees so there are no surprises later.

- Sezzle Keeps It Simple: Sezzle stands out as an interest-free option with the added potential to build credit through on-time payment reporting.

- Affirm Fits Bigger Purchases: Affirm can be a good fit for larger purchases with longer repayment plans, but some offers may include interest.

- PayPal Adds Convenience: PayPal Pay Later is easy for existing users, though monthly plans may come with interest.

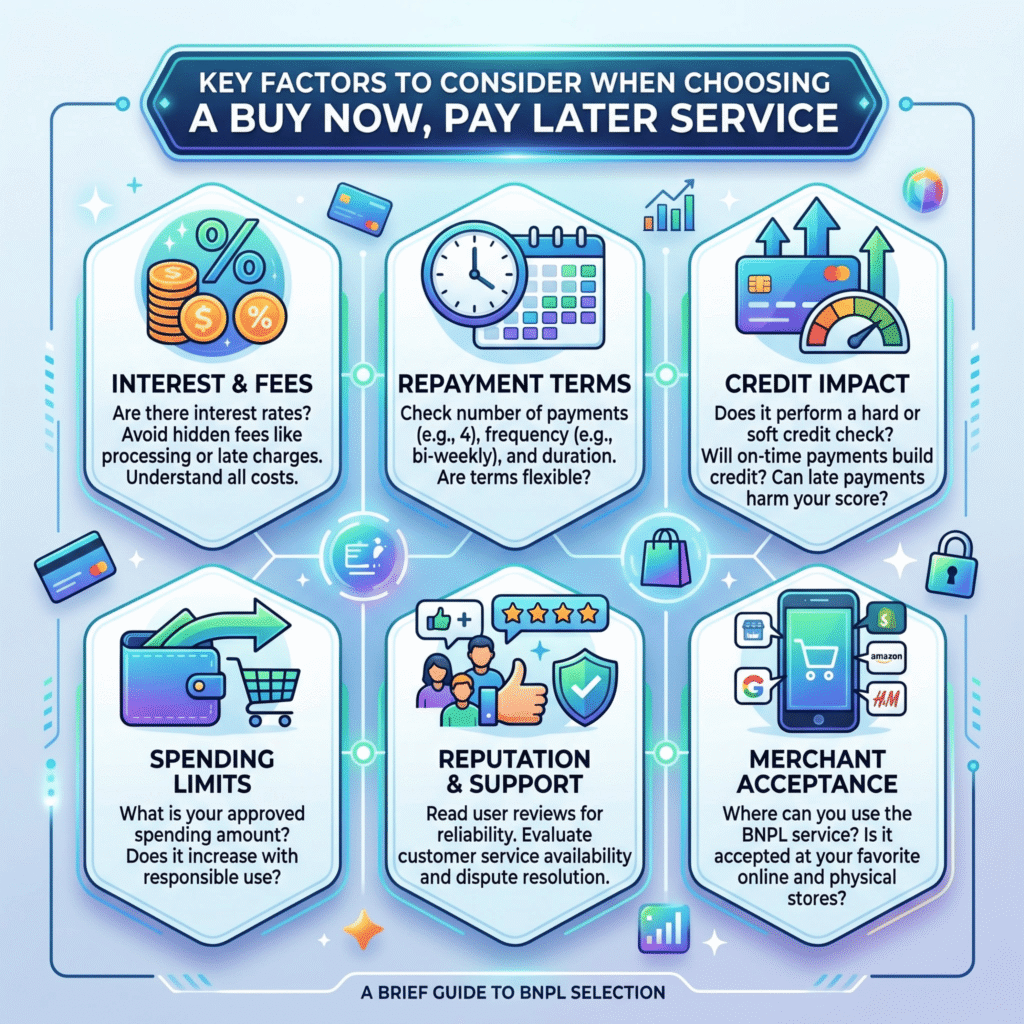

What To Look For In Apps Like Afterpay

I’d focus on a few basics before picking any buy now, pay later app. First, check whether the plan is interest-free or if interest can show up on longer terms. Then look at late fees, store availability, and whether there’s a credit check.

A few extras matter too:

- Plan length: Some apps stick to 4 payments over 6 weeks, while others go much longer

- Credit impact: Some use soft checks, some may require approval for longer plans

- Credit building: A few apps can report on-time payments

- Transparency: You should know the total cost up front

For me, the best apps like Afterpay are the ones that feel easy to use and don’t play hide-and-seek with fees.

Sezzle

Sezzle is my favorite pick in this group. It keeps the core BNPL setup simple with 4 interest-free payments, and I like that it often doesn’t require a hard credit check for the standard plan. In my opinion, the standout feature is Sezzle Up, which can help build credit history by reporting on-time payments. That’s a pretty big deal if you want flexibility now and a stronger credit profile later.

Fact Sheet

- Plan length: 4 interest-free payments over 6 weeks

- Interest: No interest on standard plans

- Credit check: Often, there’s no hard credit check for standard use

- Credit score needed: Usually not a strict minimum for basic plans

- Credit building: Yes, through Sezzle Up

- Best for: Shoppers who want simple payments and possible credit-building benefits

Klarna

Klarna is one of the biggest names in this space, and I think that’s because it gives you more than one way to pay. You can usually choose Pay in 4, Pay in 30 days, or longer financing. That flexibility is the main draw. The trade-off is that more options can also mean more room for confusion if you’re not paying attention. I’ve experienced this myself when purchasing too many mahjong sets (my newest hobby).

Fact Sheet

- Plan length: Pay in 4, Pay in 30 days, or longer monthly financing

- Interest: Interest-free on short plans: financing may include interest

- Credit check: May apply for some financing plans

- Credit score needed: Varies by plan and approval decision

- Best for: Shoppers who want flexible payment choices

Affirm

Affirm feels more geared toward bigger purchases. If you’re buying something expensive, like furniture or tech, the longer repayment window can help. I like that it shows costs up front, which makes budgeting easier. Still, it’s not always the cheapest option because some plans can carry interest, and that can change the math pretty fast.

Fact Sheet

- Plan length: About 3 to 24 months

- Interest: 0% to 36%, depending on the plan

- Credit check: Credit approval may be required, especially for longer terms

- Credit score needed: Varies by merchant and plan

- Late fees: No late fees

- Best for: Larger purchases that need more time to repay

Zip

Zip, which some people still remember as Quadpay, keeps things pretty straightforward. It usually splits purchases into 4 payments every two weeks. That makes it feel familiar if you already like the Afterpay setup. I think its big strength is wide store support, both online and in person. On the downside, it’s more of a basic option, so you won’t get as many standout features.

Fact Sheet

- Plan length: 4 payments over about 6 weeks

- Interest: No interest on standard pay-in-4 plans

- Credit check: Can vary by approval process

- Credit score needed: Not clearly fixed: approval can vary

- Best for: People who want a simple pay-in-4 app with broad acceptance

PayPal Pay Later

PayPal Pay Later is convenient mostly because so many people already use PayPal. If you shop online a lot, that built-in access can be a huge plus. It offers Pay in 4 for smaller buys and Pay Monthly for bigger ones. I’d just be more careful here, since monthly plans may include interest. Convenience is great, but not if it sneaks extra cost into the cart. They also hold out for higher credit scores in some instances.

Fact Sheet

- Plan length: Pay in 4 over 6 weeks or monthly financing

- Interest: Pay in 4 is interest-free; Pay Monthly may include interest

- Credit check: May be required for monthly plans

- Credit score needed: Varies by plan and approval

- Best for: Existing PayPal users who want a familiar checkout option

Final Thoughts

Ultimately, there are a lot of great choices if Afterpay just isn’t the right fit for your needs. Personally, I use Sezzle. I appreciate its simplicity, mobile-app-based platform, ease of use, and helpful bonus subscriptions. However, you need to choose and use what’s best for you.

Whichever BNPL provider you end up picking, just make sure you read through the terms before you sign up and start making purchases.

FAQs

Look for interest-free plans or clear interest terms, late fee policies, store availability, credit checks, plan length, credit-building options, and transparent total costs.

Sezzle often doesn’t require a hard credit check for standard use and offers Sezzle Up, a subscription that can build credit history by reporting on-time payments.

Yes, many apps offer interest-free payments with no late fees if you pay on time, keeping costs transparent.

Sezzle stands out by offering credit-building benefits through Sezzle Up, which reports payments to credit bureaus.

Most apps use the traditional pay-in-4 method, with many offering long-term plans from 12 to 24 months.