The average cost to furnish a home starts at a whopping $10,000—and while making your house feel like a home can be worth that investment, it’s not easy on anyone’s budget.

Buy now, pay later furniture makes the furniture you need feel like less of a blow to your bank account, spreading out payments over time.

And if you play it right? You can do it interest-free.

As a BNPL user, here’s what you need to know to make the most of the service.

Key Takeaways

- Helps Spread Out Big Purchases: Buy now, pay later furniture options let you bring home larger items right away while breaking the cost into smaller payments over time.

- Short Plans Can Be Cheaper: Many BNPL furniture plans are interest-free if paid on time, though longer plans may include interest or fees.

- May Cover More Than The Item: Depending on the retailer, the payment plan may also apply to things like shipping, assembly, or protection plans.

- The Right Plan Depends On The Full Cost: It’s worth comparing payment size, repayment length, total cost, and any extra fees before choosing a plan.

- Works Best As A Cash-Flow Tool: BNPL for furniture is most useful when it helps reduce budget stress, not when it pushes you into buying more than you can comfortably afford.

What Buy Now, Pay Later Furniture Means

Buy now, pay later furniture means you can bring home furniture now and split the cost into fixed payments instead of paying the whole amount at checkout. Usually, the store gets paid upfront by the financing partner or through store financing, and you repay in installments.

This can apply to common purchases like couches, beds, mattresses, desks, dining tables, bookshelves, and accent chairs. Sometimes it also covers extras tied to the order, like shipping, assembly, installation, and protection plans, but that depends on the retailer and the plan terms, so I always check before clicking buy.

Personally, I love to shop for antiques and thrift my furniture and since layaways are mostly a thing of the past, BNPLs are a way to make sure that no one else takes my dream china cabinet while I wait to save the money.

How Furniture Payment Plans Usually Work

Most furniture payment plans are simple. At checkout online or in-store, I choose a pay-over-time option, enter a few details, and get a quick approval decision. Short plans often use a soft credit check, while longer financing can be stricter.

A common setup is pay in 4: 25% due now, then three equal payments every two weeks. Here’s what that might look like:

| Furniture item | Example price range | Pay-in-4 payment |

|---|---|---|

| Couch | $500–$1,000 | $125–$250 |

| Dining table | $300–$800 | $75–$200 |

| Bed frame | $250–$700 | $62.50–$175 |

| Bookshelf | $120–$400 | $30–$100 |

| Accent chair | $150–$500 | $37.50–$125 |

Sezzle is my favorite provider for buying furniture, because they have an impressive partner list, virtual cards that let you use BNPL in physical, in-person stores, and unique opportunities for earning rewards, like Sezzle Spend.

Common Costs, Interest, And Credit Requirements

This is where buy now, pay later furniture can be either helpful or sneaky. Short pay-in-4 plans are often 0% interest when paid on time. Longer monthly plans may charge interest, and that rate can range from low to very expensive depending on credit and the retailer.

Also, watch for late fees, account fees, and deferred-interest offers. Deferred interest is the one that bites people: if the balance isn’t cleared in time, interest can hit retroactively. Credit requirements vary, too. Some plans use soft checks, while store credit accounts may involve a hard pull and stricter approval standards.

Where You Can Use Buy Now, Pay Later For Furniture

You can use buy now, pay later for furniture at a lot of places now, both online and in person. Large retailers, furniture chains, department stores, home improvement stores, and marketplace-style sites often offer some version of split payments or monthly financing at checkout.

That includes stores selling sofas, mattresses, office furniture, patio sets, and storage pieces. In many cases, BNPL applies to the full cart total, not just the furniture itself. So yes, shipping charges, white-glove delivery, setup, assembly, and even warranties may be included if they’re part of the checkout total. But not always. Verify that before assuming the full order is covered.

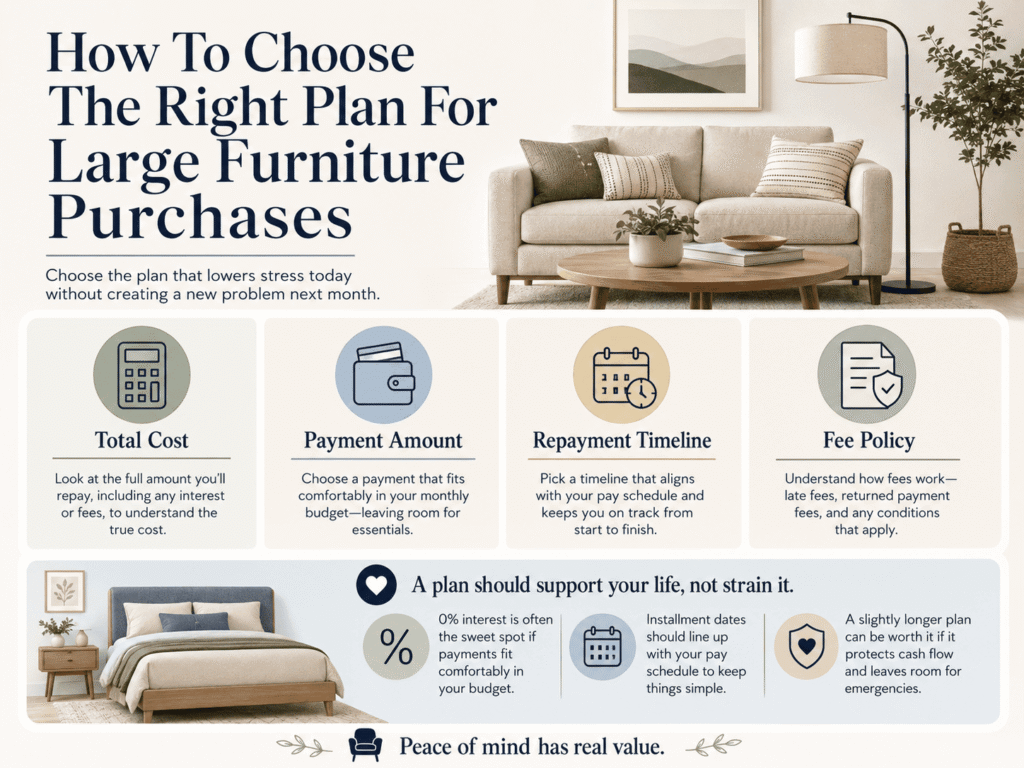

How To Choose The Right Plan For Large Furniture Purchases

For me, the best plan is the one that lowers stress without creating a new problem next month. I compare four things: the total cost, the payment amount, the repayment timeline, and the fee policy.

If you can get 0% interest and the payments fit comfortably into my budget, that’s usually the sweet spot. Also, make sure the installment dates line up with my pay schedule. A slightly longer plan can be worth it if it protects my cash flow and leaves room for emergencies. Peace of mind has real value, especially when money already feels tight.

Risks To Watch Before You Check Out

I’m pro-BNPL, but only when I’m honest with myself. The biggest risk is treating smaller payments like smaller costs; they’re not. It’s still the same purchase, just spread out.

I also watch out for stacking multiple plans at once. A couch payment here, a desk payment there, and suddenly next month’s budget is crowded. Missing a payment can mean fees, lost promo terms, or even credit damage in some cases. Before checkout, I look at the full schedule, not just today’s payment. If the future version of me would feel squeezed, I wait.

Bottom Line

Buy now, pay later furniture makes sense when I could afford the purchase outright but want to protect my breathing room. Used carefully, it’s less about overspending and more about reducing stress, smoothing cash flow, and keeping one big purchase from wrecking an otherwise normal month.

FAQs

What does buy now, pay later furniture mean?

Buy now, pay later furniture lets you take furniture home immediately and pay over time in fixed installments, often through a financing app or store credit instead of paying the full amount upfront.

How do furniture buy-now, pay-later payment plans usually work?

At checkout, you select a BNPL option, complete a quick approval often involving a soft credit check, then pay the initial installment with the remaining payments spread over weeks or months, commonly in four equal parts.

Do BNPL furniture plans charge fees or interest?

Short-term plans like pay-in-4 often have 0% interest if paid on time, but longer terms may charge interest rates from low up to 30% APR, plus potential late fees or deferred-interest penalties if payments are late or missed.

Where can I use buy now, pay later options to purchase furniture?

BNPL furniture financing is available at many retailers, including Wayfair, IKEA, Target, Home Depot, Overstock, and others, both online and in-store, often covering the full order, including shipping or assembly fees, depending on terms.

What should I consider when choosing a buy-now, pay-later furniture plan?

Compare total costs including interest and fees, ensure monthly payments fit your budget, check the repayment timeline, and prefer plans with 0% APR and clear fee policies to protect your cash flow and avoid stress.

What are the risks of using buy now, pay later for furniture purchases?

Risks include accumulating high interest if not paid on time, late fees, negative credit reporting from missed payments, and overspending by managing multiple BNPL plans simultaneously, which can strain your monthly budget.