If you’re thinking about using Sezzle, it can be easy—and even smart—to worry that it’s too good to be true. Surely, you’ll rack up interest… right?

Well, according to CNBC, BNPL companies like Sezzle usually make the largest bulk of their revenue from retailers, but that doesn’t mean interest isn’t a factor.

I’ve used Sezzle myself, and in the article to follow, I’ll walk you through whether Sezzle charges interest, how much it is when they do, and how to stay on the straight and narrow so interest isn’t a concern.

Key Takeaways

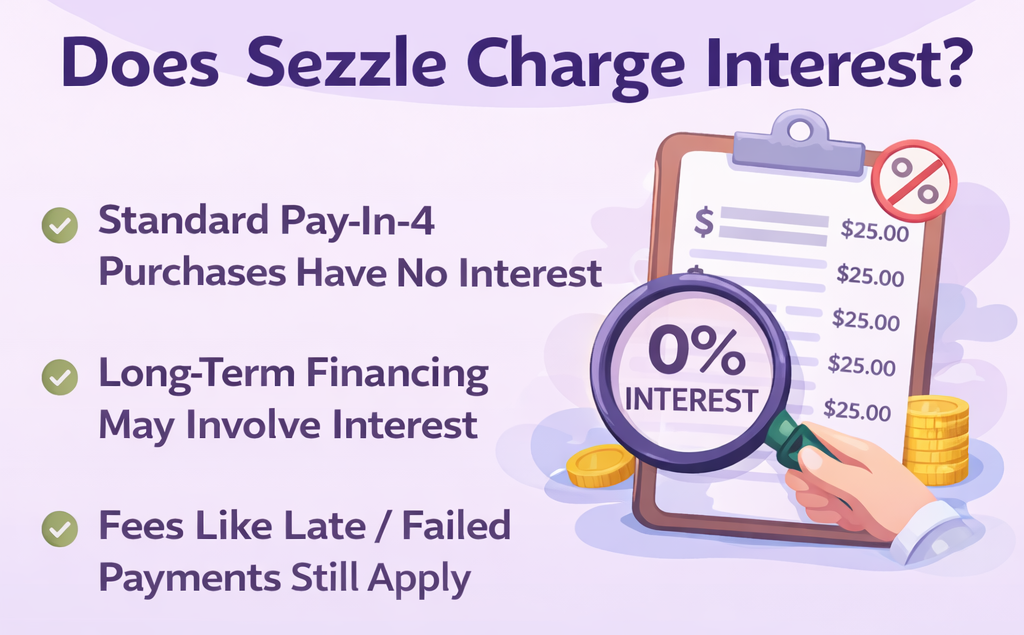

- Standard Plans Are Usually Interest-Free: Sezzle’s Pay in 4 and Pay in 5 options usually do not charge interest on standard purchases.

- Fees Can Still Apply: Even without interest, some Sezzle transactions may include service fees, late fees, failed payment fees, or other charges.

- Monthly Financing Is Different: Longer-term payment plans are not the same as Pay in 4 and may involve interest through a lending partner.

- Paying On Time Matters: If you make your payments on time, Sezzle can be a helpful way to split purchases without typical credit card interest.

- Always Check The Terms: Before you buy, look for service fees, APR, and lender disclosures so you know the true cost of the purchase.

Does Sezzle Charge Interest? The Short Answer

For standard Sezzle purchases, you probably won’t have to worry about interest.

Sezzle’s Pay in 4 and Pay in 5 plans offer interest-free payment options. These are the plans most people mean when they talk about using Sezzle at checkout, and the plans you’d be most likely to use. So if you’re splitting a smaller purchase into a few payments, interest usually isn’t the thing you need to worry about most.

What Pay in 4 Actually Means

With standard Pay in 4, the purchase is split into smaller payments over a short period.

That’s what makes it appealing. You don’t have to pay the full amount all at once, but you also aren’t dealing with traditional credit card interest if everything goes smoothly.

For people who want flexibility without dragging a balance out for months, that can be a real plus.

That’s also why a lot of users like it. When it’s used responsibly, it can feel more like a budgeting tool than a debt product.

My Experience With Sezzle

I’ve used Sezzle’s Pay in 4 plan myself, and interest was never an issue for me.

That’s because I used the standard installment option and paid on time. In that setup, it was pretty straightforward and genuinely useful. I think that’s an important point. Sezzle tends to work best when you use it for short-term breathing room, not as an excuse to buy things you really can’t afford.

Also, if you are a Sezzle Anywhere member, service fees do not apply.

No Interest Doesn’t Mean No Fees

This is the part I really hope you’re paying attention to! If you read a single section in this article, read this one.

Sezzle says some purchases can come with other charges, even if they don’t include standard interest.

Those can include:

- Service fees

- Failed payment fees

- Late payment fees

- Reschedule fees

- A Late Saver Fee in some cases

So yes, a Sezzle purchase can sometimes cost more than the sticker price.

What a Service Fee Means

Sezzle says a service fee is a prepaid finance charge.

That fee can apply to some transactions, including certain single-use virtual card purchases. It may be added upfront and shown before checkout.

So, if you see a service fee or APR, you shouldn’t think of the purchase as a simple free payment split. At that point, it’s a cost-bearing financing product.

The Virtual Card Detail Matters

The virtual card is one area where fees can show up.

That doesn’t mean every virtual card transaction comes with interest or extra cost. But it does mean you should pay attention if you’re using that feature.

If Sezzle shows a fee before checkout, that fee is part of the total cost. It’s not something to ignore just because the brand is often associated with interest-free payments.

Pay in 4 and Monthly Financing Are Not the Same

Sezzle’s standard Pay in 2, Pay in 4, and Pay in 5 plans are not the same as its longer-term monthly financing options.

The short-term plans are the ones Sezzle describes as no-interest.

Monthly financing is different. Sezzle says longer-term financing may be offered through lending partners such as Bread Financial. It also says paying those plans off early can reduce the amount of interest paid over time.

That means interest may be involved in those longer plans.

So, Can Sezzle Charge Interest?

Yes, in some cases.

If you’re using the standard Pay in 4 or Pay in 5 option, usually not. If you’re using a longer-term monthly financing offer, interest may apply. That’s why the most accurate answer is not just “yes” or “no.” It depends on what type of Sezzle product you’re actually choosing.

How to Check Before You Buy

The best thing you can do is slow down for a second before completing the purchase.

Check the details on the screen and look for anything that changes the cost.

Pay attention to whether:

- It’s Pay in 4 or monthly financing

- A service fee is listed

- An APR appears

- There’s a lender disclosure

If the checkout page shows extra costs, take that seriously.

Is Sezzle Still Worth Using?

For a lot of people, yes.

If you use the standard plan, pay on time, and know what you’re agreeing to, Sezzle can be a helpful option. It gives you flexibility without the usual interest that comes with many credit cards.

That’s why I think it can be a solid tool when it’s used responsibly.

My own experience has been positive, but that’s because I stayed in the lane where Sezzle works best: short-term payments, on-time payments, no surprises.

The Honest Bottom Line

Sezzle usually does not charge interest on standard Pay in 4 or Pay in 5 purchases, but that doesn’t mean every Sezzle transaction is free of extra cost.

If you read the checkout details and stick to the standard short-term plan, however, Sezzle can be a useful and convenient payment tool. If you ignore the terms, it can get more expensive than expected.

That’s really the whole story!

Used responsibly, Sezzle can be helpful. Just make sure you know which version of Sezzle you’re using before you click “buy now.”

FAQs

Usually, no. Sezzle says its standard Pay in 4 plan is a no-interest option, as long as you’re using the standard installment product.

Yes. Even if a plan has no interest, extra costs can come from service fees, late fees, failed payment fees, or other charges.

For standard plans, Sezzle generally describes the added cost as fees rather than traditional interest. Missing a payment can still make your purchase more expensive.

They can. Sezzle’s longer-term financing options may involve interest through a lending partner, which makes them different from Pay in 4.

Check the checkout screen and any loan disclosures before confirming the order. If you see a service fee, APR, or lender terms, the purchase may cost more than the item price.