It’s critical to know how your payment history is affecting your credit score, whether positively or negatively. After all, according to Experian—one of the “big three” credit bureaus—your payment history accounts for the largest percentage of any factor at 35%.

So naturally, when I was considering using a Pay-in-4 plan from Sezzle to help with a trip I was taking with my family, I wanted to know whether Sezzle reported to credit bureaus.

So, based on my research and personal experiences using Sezzle, here’s what you need to know about the BNPL service and how it interacts with credit bureaus.

Key Takeaways

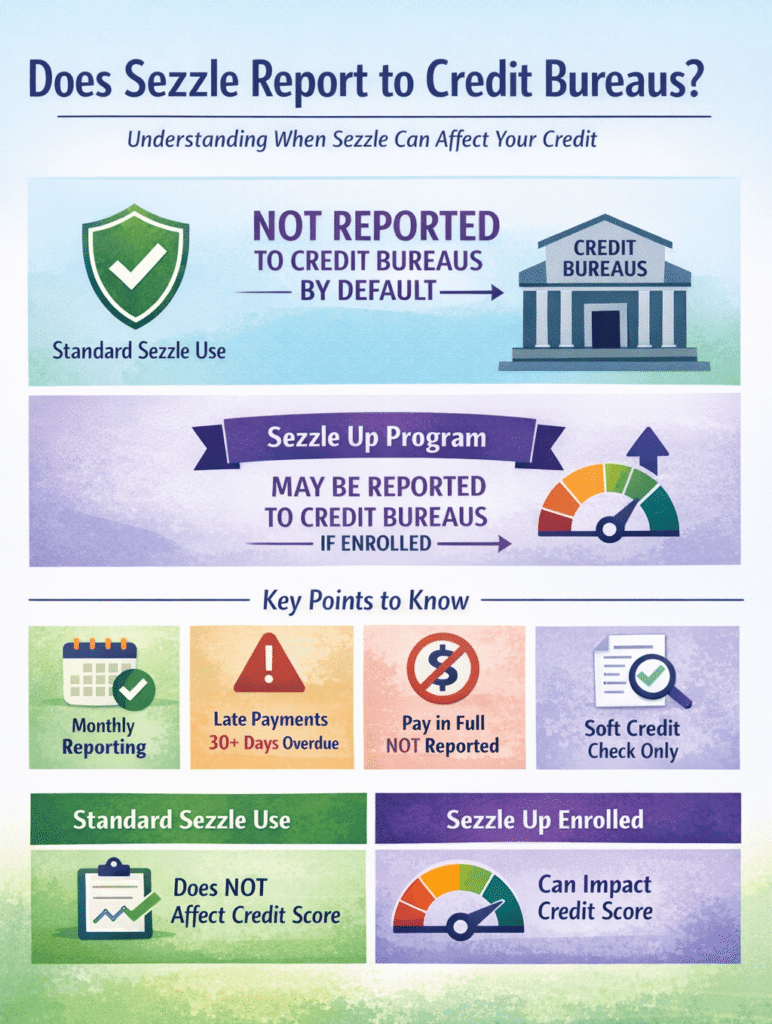

- Sezzle Does Not Report By Default: Standard Sezzle use is not automatically reported to credit bureaus.

- Sezzle Up Is The Exception: If you enroll in Sezzle Up, Sezzle may report payment history to one or more credit bureaus.

- Reporting Happens Monthly: Sezzle says credit reporting through Sezzle Up is done on a monthly basis, not in real time.

- Not Every Transaction Counts: Sezzle says Pay in Full transactions are not reported through Sezzle Up.

- Late Payments May Be Reported: For users enrolled in Sezzle Up, late or failed payments that are 30 days or more overdue may be reported, and there is no way to “unreport” them later.

The Main Thing to Know

Sezzle does not report standard user activity to credit bureaus by default.

If you use Sezzle the typical way, your payment history usually isn’t sent to the credit bureaus. For many shoppers, that’s actually part of the appeal. It lets you split up payments without turning every purchase into a credit event.

The tradeoff is that this kind of usage doesn’t typically help build your credit history either.

A lot of the confusion comes from how people ask the question. There are really two different things to consider:

- Does Sezzle report by default?

- Can Sezzle report under certain conditions?

The answer to the first is no. The answer to the second is yes.

That’s where broad statements tend to fall short. Saying Sezzle “doesn’t report” isn’t completely accurate. It just doesn’t report in the way most people assume.

The Exception: Sezzle Up

Sezzle Up is Sezzle’s optional credit-building program.

If you enroll in it, Sezzle says it may report your payment history to one or more nationwide credit bureaus. That changes the answer in a big way. Once you opt in, Sezzle can become part of your credit story in a way it usually doesn’t for standard users.

That’s the distinction that matters most.

What Sezzle Up Changes

When you enroll in Sezzle Up, Sezzle says a few important things happen:

- Your qualifying payment history may be reported

- Reporting happens monthly, not instantly

- Late or failed payments that are 30 days or more overdue may be reported

- Pay in Full transactions are not reported through the program

So Sezzle Up is not a small side feature. It changes how your account may connect to the credit system.

What Sezzle Up Does Not Mean

It does not mean every Sezzle transaction will automatically help build your credit history.

It also does not mean every purchase type is treated the same way.

Another important detail is that once you enroll in the credit-building program, you can’t simply turn it off later. That decision tends to stick, which makes it something you should think through before opting in.

That’s where people sometimes oversimplify things. They hear “credit-building program” and assume all Sezzle activity suddenly becomes credit-building activity. That’s not the safest way to look at it.

What This Means for the Average User

For most people, the takeaway is pretty simple.

If you’re just using Sezzle in the standard way, it usually won’t be reported to credit bureaus. That means it usually won’t hurt your credit just by existing, but it also usually won’t help build your credit either.

If you want reporting to happen, you’d need to enroll in Sezzle Up.

I think that setup makes sense. Some people want the flexibility of buy now, pay later without involving their credit report. Others want the chance to build payment history. Sezzle seems to separate those two paths rather than forcing everyone into one system.

Can Sezzle Help Build Credit History?

Potentially, yes.

But only if you’re enrolled in Sezzle Up, and the payment activity qualifies for reporting. That’s the key condition. Without that program, regular Sezzle use does not automatically build your credit through bureau reporting.

So if your goal is credit building, don’t assume Sezzle is helping just because you’re paying on time. You need to know whether you’re actually enrolled in the reporting program first.

That’s the piece many people skip.

What About Late Payments?

This part matters just as much as the credit-building angle.

Sezzle says late or failed payments that are 30 days or more overdue may be reported for users enrolled in Sezzle Up. So the reporting feature is not just about the upside. It can also create a downside if payments are missed and stay unpaid for long enough.

That doesn’t mean every late payment is treated the same way in every situation. But it does mean Sezzle Up should be taken seriously.

If someone wants the possible credit benefit, they also need to be ready for the fact that negative behavior may matter too.

A Quick Note on Credit Checks

Sezzle may use a soft credit check to determine spending power.

That’s worth pointing out because people often hear “credit check” and immediately assume the worst. But a soft inquiry is not the same as a hard inquiry. Sezzle says a soft credit check does not negatively affect a credit score.

So in this case, a credit check does not automatically mean credit damage.

Before You Assume Anything, Check These Details

If you’re trying to figure out whether Sezzle will affect your credit, these are the questions to ask:

- Are you using standard Sezzle or Sezzle Up?

- Is the transaction a Pay in Full purchase?

- Are you expecting reporting to happen right away?

- Are you assuming on-time payments count without checking the program terms?

- Are you aware that seriously late payments may be reported if you’re enrolled?

That short checklist clears up most of the confusion.

The Bottom Line

Sezzle does not report to credit bureaus by default. That’s the answer most users need.

The reason people get tripped up is Sezzle Up. If you enroll in that optional credit-building program, Sezzle may report payment history monthly to one or more nationwide credit bureaus. Sezzle also says Pay in Full transactions are not reported through Sezzle Up, and late or failed payments that are 30 days or more overdue may be reported for enrolled users.

So if you want the cleanest way to think about it, here it is: standard Sezzle usually stays off your credit report, while Sezzle Up may bring reporting into the picture. That one difference is what changes the answer.

FAQs

No. Sezzle says standard use is not reported to credit bureaus by default.

Sezzle Up is Sezzle’s optional credit-building program. If you enroll, Sezzle may report payment history to one or more nationwide credit bureaus.

It may, but only if you’re enrolled in Sezzle Up, and your qualifying payment history is reported. Standard Sezzle use does not automatically build credit through bureau reporting.

They may if you’re enrolled in Sezzle Up. Sezzle says late or failed payments that are 30 days or more overdue can be reported for enrolled users.

No. Sezzle says Pay in Full transactions are not reported as part of Sezzle Up.