You can go to Lowe’s for one thing and somehow end up staring at a cart total that is….

Well, very much not a “one thing” price.

That’s usually when Lowe’s buy now, pay later options start sounding a lot more interesting.

The problem is that Lowe’s doesn’t really have one simple pay-later setup. It has a couple of different ways to spread out a purchase, and they don’t all work the same way.

So, I went through Lowe’s current options to sort out what’s actually BNPL, what’s really store-card financing, and where third-party BNPL providers fit in.

Key Takeaways

- Lowe’s Has More Than One Option: Lowe’s Pay, the store card, and third-party BNPL services all work differently.

- Lowe’s Pay Is The Closest Match To BNPL: It’s the most direct pay-over-time option built into Lowe’s setup.

- The Store Card Isn’t Typical BNPL: It’s really store financing, and the promo details matter.

- Deferred Interest Can Get Expensive: If you miss the payoff window, interest can go all the way back to the purchase date.

- Sezzle Works More Like A Workaround: You can still use it, but it’s not Lowe’s main checkout option.

The Quick Answer

Yes, Lowe’s does offer pay-over-time options, but there are a few separate lanes:

- Lowe’s Pay, which is Lowe’s own BNPL-style option and is offered through Synchrony Pay Later

- Affirm, which Lowe’s also lists as a pay-over-time option

- The MyLowe’s Rewards Credit Card, which is more traditional store financing than classic BNPL

- Sezzle, which can still work through the Sezzle app or virtual card, rather than as Lowe’s main built-in checkout option

If you’re trying to figure out which one matters most, I’d pay the closest attention to Lowe’s Pay and the MyLowe’s Rewards Credit Card. Those are the two that tell you the most about how Lowe’s wants people to finance purchases on its own site.

Lowe’s Pay Is the Closest Thing to Built-In BNPL

Lowe’s Pay is the cleanest answer to the question, “Does Lowe’s have buy now, pay later?” Lowe’s lets customers pay in equal monthly installments over 3, 6, 12, 18, or 24 months, and it’s financed and underwritten by Synchrony Bank through Synchrony Pay Later.

A few details here are actually useful:

- You can prequalify for flexible financing options with no impact on your credit bureau score.

- Terms depend on credit approval and order total.

- Lowe’s Pay transactions do not qualify for Lowe’s credit promotions, such as 5% off or special financing.

That last point is the one I’d notice. Lowe’s Pay is straightforward, but it’s separate from the store-card promos people often compare it to.

The MyLowe’s Rewards Credit Card Isn’t Really BNPL

This is where things get confusing fast.

The MyLowe’s Rewards Credit Card is not the same thing as a standard BNPL checkout option. It’s a store credit card with a mix of everyday discounts, deferred-interest promos, and longer fixed-payment offers.

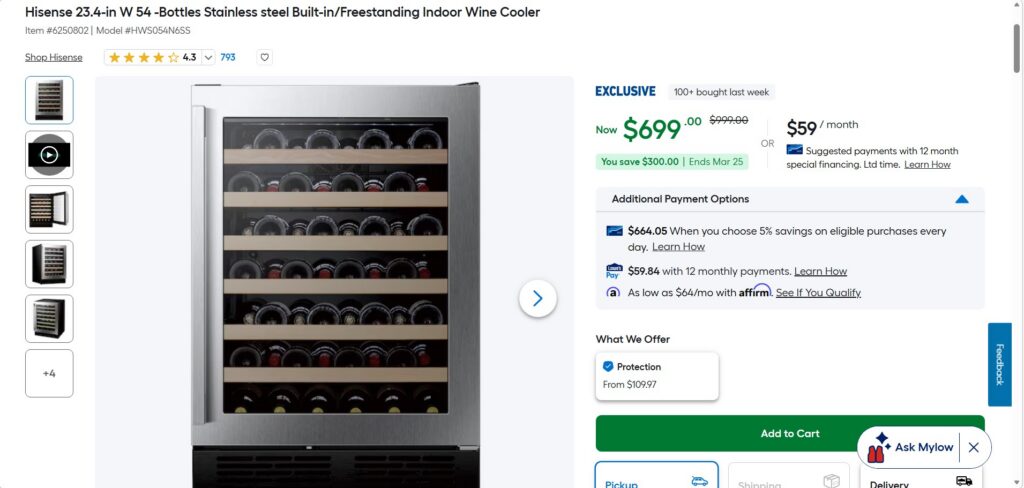

Lowe’s currently highlights features such as 5% off eligible purchases, no interest if paid in full within 12 months on purchases of $299 or more, and fixed monthly payment offers on qualifying larger purchases.

That can still be useful. It just works differently, and the details matter a lot more than the headline.

The Appliance Financing Detail People Should Actually Know

This is the part I’d want spelled out clearly if I were deciding whether to use the card.

For appliances, Lowe’s says cardholders can get no interest if paid in full within 12 months on purchases of $299 or more. But that is a deferred-interest promo, not a casual “pay over time and don’t worry about it” deal. If the promotional purchase is not paid in full within 12 months, Lowe’s says interest is charged from the original purchase date. Minimum monthly payments are still required the whole time.

Lowe’s also explains that the suggested equal monthly payment is meant to pay off the promo balance within the 12-month window, but that amount can be higher than the minimum payment on the billing statement. In plain English, paying the minimum may not be enough to avoid interest.

That’s a big difference from the way a lot of people think about BNPL. If you use the store card for one of these promos, you really have to know what kind of financing you’re signing up for.

What the Store Card Offers Beyond That

On bigger purchases, Lowe’s also advertises fixed monthly payment promotions on the MyLowe’s Rewards Credit Card. Right now, Lowe’s lists 36 payments at 7.99% APR, 60 at 8.99% APR, and 84 at 9.99% APR for qualifying purchases of $2,000 or more, with the 36- and 60-month offers limited to installed sales.

That doesn’t automatically make the card a bad option. It just means this is closer to traditional financing than the kind of quick BNPL setup people usually have in mind.

Can You Use Sezzle at Lowe’s?

Yes, but it helps to think of Sezzle as something you bring to Lowe’s, not something Lowe’s is really pushing.

Sezzle has a Lowe’s page that tells shoppers to use the Sezzle app, create a single-use virtual card, and enter that card at checkout. Sezzle says the purchase is then split into four interest-free payments over six weeks.

That means Sezzle can still be a practical option if that’s the service you already like using. It just isn’t the main BNPL button Lowe’s is putting front and center on its own payment pages.

What I’d Pay Attention to Before Choosing One

If you’re comparing Lowe’s pay-later options, these are the questions that matter most:

- Is this actual BNPL, or is it store-card financing?

- Does the offer involve deferred interest?

- Will the minimum payment really pay the balance off in time?

- Do you lose access to 5% off or other promos by choosing Lowe’s Pay?

- Are you using Lowe’s built-in option, or a workaround like Sezzle?

That’s really the split here. Lowe’s Pay is more of a straight BNPL-style route. The MyLowe’s Rewards Credit Card can be useful, but it comes with more moving parts. And Sezzle is still a powerful option, just not the one Lowe’s leads with.

Bottom Line

Lowe’s does offer a few different ways to pay over time, but they’re not interchangeable. Lowe’s Pay is the closest thing to a standard BNPL option, the MyLowe’s Rewards Credit Card works more like traditional store financing, and Sezzle is there if you prefer using a virtual card.

That’s really what matters here. Before you choose one, make sure you understand how that specific option works, what it may cost, and whether it actually fits the purchase you’re making.

FAQs

Yes. Lowe’s offers Lowe’s Pay for pay-over-time purchases, and shoppers may also come across other financing routes depending on how they check out.

No. Lowe’s Pay is the closer match to a standard BNPL option, while the MyLowe’s Rewards Credit Card is store financing with promo terms.

Yes. Lowe’s offers Affirm as one of its pay-over-time options, but it’s not the only route shoppers can use.

Yes, but usually through the Sezzle app or virtual card rather than as Lowe’s main built-in checkout option.

The deferred-interest promos. If you don’t pay the balance in full within the promo window, interest can be charged from the original purchase date.