Buy now, pay later did not become popular because people forgot how money works. It became popular because a lot of people looked at their credit cards and thought, there has to be a simpler way to do this.

So, what is buy now, pay later? It’s a payment method that lets shoppers split a purchase into smaller payments instead of paying everything up front or carrying a balance for months.

That’s the definition. The reason people use it is more practical than that.

Key Takeaways

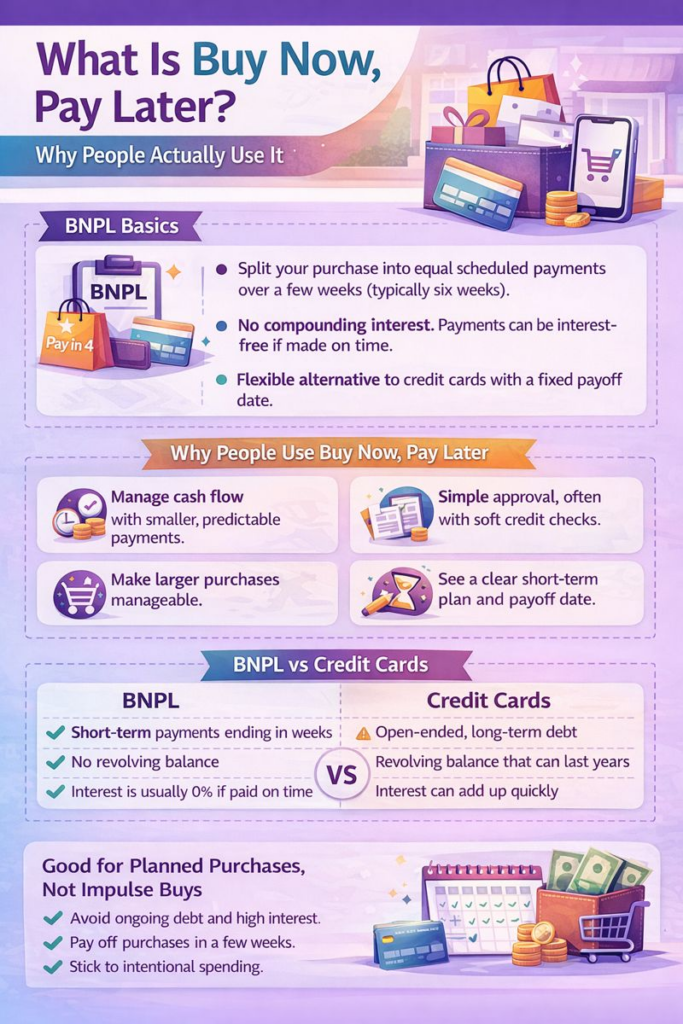

- Buy now, pay later breaks purchases into short-term payments. Most plans use equal installments paid over a few weeks, often around six weeks.

- Many BNPL plans offer interest-free payments. As long as payments are made on time, most providers do not charge interest.

- BNPL is not the same as credit cards or traditional loans. Payments end on a fixed timeline instead of rolling into ongoing debt.

- Credit impact depends on the provider and your payment behavior. Some BNPL services report payment history, while missed payments can still lead to fees or restrictions.

- Buy now, pay later works best for planned purchases. It helps with timing and cash flow, not long-term borrowing.

Buy Now, Pay Later Exists Because Credit Got Complicated

Credit cards are powerful tools, but they come with APRs, grace periods, credit limits, and the temptation to carry a balance longer than planned. Even people who pay off credit cards regularly still have to manage interest rates and due dates.

Buy now, pay later simplifies that experience. Instead of open-ended consumer credit, it offers a short-term structure. You see the payment plan before checkout. You know when the payments end. There’s no guessing how long the purchase will linger.

For many BNPL users, that clarity is the appeal.

What a Buy Now, Pay Later Plan Looks Like in Real Life

Most buy now, pay later plans follow a simple flow:

- You choose buy now, pay later at checkout

- You make the first payment or down payment

- The remaining amount is split into equal installments

- Payments finish in a few weeks

These pay-in-four loans often come with zero interest if payments are made on time. There’s no compounding interest and no revolving balance, which makes costs easier to manage.

Is Buy Now, Pay Later a Loan?

Most BNPL plans are installment loans, but they don’t behave like traditional loans. The application process is quick, approval is often based on soft credit checks, and many providers, such as Sezzle and Klarna, rely on internal payment history rather than deep credit reviews.

Some BNPL lenders report payment history to credit bureaus, while others keep BNPL credit separate. That means your credit score may or may not be affected, depending on the provider and how consistently you make payments.

Late payments can still trigger late fees or service fees, even on interest-free plans.

Why People Use Buy Now, Pay Later for Larger Purchases

Buy now, pay later works best for purchases that feel too big to pay all at once but too small to justify long-term financing.

Spreading payments over a few weeks helps manage cash flow without adding to credit card debt. That’s why BNPL has become popular for online shopping, major purchases, and situations where timing matters more than rewards points.

It’s an alternative financing option, not a replacement for all forms of credit.

The Biggest Misunderstanding: “It’s Free Money”

Buy now, pay later is not free money. It just feels lighter because payments are smaller.

Late fees, additional fees, and missed payments can still cause problems. Loan stacking, where multiple BNPL plans overlap, can quietly strain a tight budget if repayment dates pile up.

Most BNPL providers limit credit and monitor outstanding loans to reduce risk, but responsible use still matters.

Buy Now, Pay Later vs Credit Cards

Credit cards are designed for ongoing access to credit.

Buy now, pay later is designed for short-term follow-through.

That difference explains why BNPL appeals to consumers who want clear repayment terms instead of long-term balances.

Buy now, pay later works well when:

- You have a specific purchase in mind

- You can comfortably handle scheduled payments

- You want interest-free installments over a short period

It works poorly when:

- Payments are missed frequently

- Multiple BNPL loans overlap

- It replaces budgeting instead of supporting it

The Bottom Line: What BNPL Is Really For

Buy now, pay later is a tool for managing timing, not increasing spending power. It gives consumers a way to spread costs over a few weeks without relying on compounding interest or long-term loans.

Used intentionally, BNPL can reduce reliance on credit cards and make larger purchases feel manageable. Used carelessly, it creates the same stress as other forms of consumer credit.

The structure is simple. The choices still matter.

FAQs

Buy now, pay later is a payment method offered by BNPL providers that lets shoppers use short-term BNPL loans to split purchases into equal installments over a few weeks, often with interest-free payments instead of traditional consumer credit.

Buy now, pay later can affect a customer’s credit score depending on the BNPL service, whether payment history is reported to credit bureaus, and if missed payments, late fees, or loan stacking occur across multiple BNPL lenders.

Buy now, pay later can affect your credit score depending on the provider, whether payments are reported, and whether payments are made on time.

Buy now, pay later can be better for short-term purchases with clear repayment plans, while credit cards may be better for long-term or recurring expenses.

Buy now, pay later services typically link to a bank account or debit card to schedule automatic payments, and data referenced by the Federal Reserve Bank shows that this direct repayment model helps limit compounding interest compared to traditional credit cards.