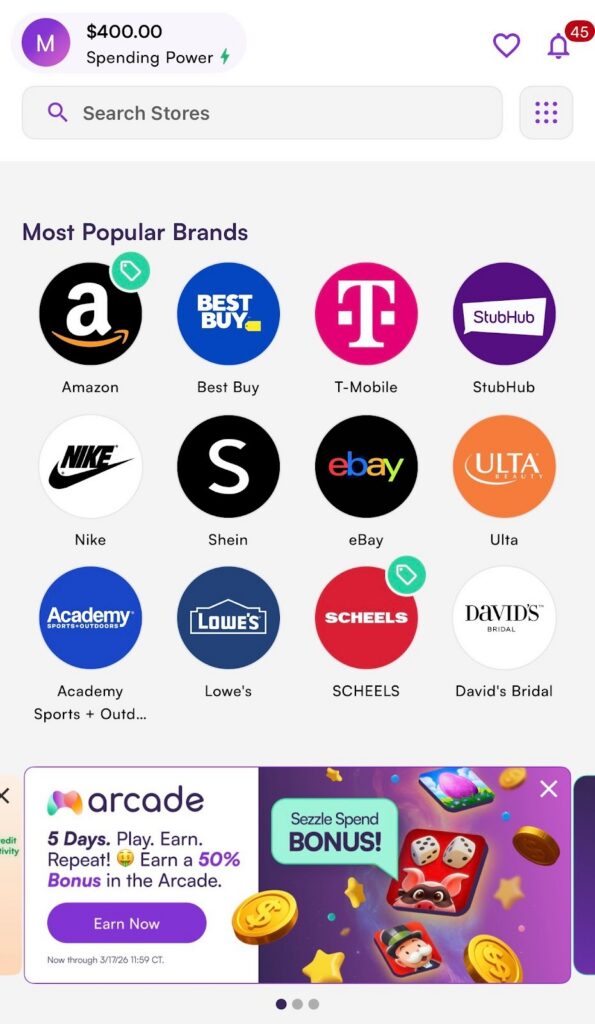

Sezzle is everywhere now—especially if you shop online—and over 3 million users have hopped on board (including yours truly). You see it at checkout next to your other payment options, usually with a simple pitch: split your purchase into smaller payments instead of paying the full amount upfront.

That convenience is a big reason Sezzle has become so popular, and a reason why I’ve continued to use it for years. But the easy checkout pitch doesn’t tell you much about what Sezzle actually is, how it works, or when it makes sense to use.

If you’re wondering whether Sezzle is basically a credit card, a short-term payment tool, or something in between, the answer starts right here.

Key Takeaways

- Sezzle Is A BNPL Service: Sezzle is a buy now, pay later platform that lets shoppers split eligible purchases into smaller payments over time.

- It Adds Checkout Flexibility: Instead of paying the full amount upfront, shoppers can use Sezzle to spread out the cost on a set schedule.

- It Is Not The Same As A Credit Card: Sezzle is usually tied to a specific purchase rather than a revolving credit line you keep using.

- It Can Help Or Hurt: Used responsibly, Sezzle can support cash flow. Used carelessly, it can make overspending easier.

- The Terms Still Matter: Before using Sezzle, shoppers should understand payment timing, account terms, and how the plan fits their budget.

What Is Sezzle? The Short Version

If you want the fast answer, here it is:

- Sezzle is a buy now, pay later platform

- It lets you split purchases into smaller payments

- It is commonly used at online checkout

- It is designed to give shoppers more payment flexibility

- It is not exactly the same as a credit card

How Sezzle Works

At a high level, Sezzle steps in at checkout and gives you a different way to pay.

Instead of paying the full purchase price right away, you choose Sezzle, go through its approval process, and agree to a payment schedule. From there, the total cost is broken into installments. The exact offer can depend on the purchase and the account, but the core idea stays the same: Sezzle lets you spread out the cost instead of paying everything up front.

For shoppers, that can make checkout feel a lot easier. For budgets, it can be helpful too, at least when the payment dates and amounts are realistic.

Why People Use Sezzle

The biggest reason is simple: cash flow.

Sometimes a person can afford something, but not comfortably all at once. Breaking the purchase into smaller payments may make it easier to fit into a weekly or biweekly budget.

People often use Sezzle because they want to:

- Spread out the cost of a purchase

- Avoid a large one-time charge

- Line up payments with payday timing

- Get flexibility without using a traditional credit card

- Make checkout feel more manageable

That doesn’t automatically mean Sezzle is the right choice for every purchase. But it does explain why it has become such a familiar option.

What Sezzle Is (and What It Isn’t)

One reason people get confused about Sezzle is that they try to compare it to products that don’t work exactly the same way. Sezzle is not just “a credit card without the plastic.” It’s also not the same as paying cash. It sits somewhere in between.

Here’s the easiest way to think about it:

Sezzle Is:

- A buy now, pay later payment option

- A way to split eligible purchases into installments

- A tool for short-term payment flexibility

Sezzle Is Not:

- The same thing as a revolving credit card

- A guarantee that every purchase is free of extra costs

- A reason to stop paying attention to your budget

As someone who’s used Sezzle plenty of times, I’d argue that the middle-ground framing is the most accurate. Sezzle is a payment tool, not a magic trick. It can make timing easier, but it does not erase the fact that the money still has to come from somewhere. It’s about stretching your paycheck further over time, not pulling money that doesn’t exist out of thin air.

Why Sezzle Can Feel So Easy to Use

This is part of the appeal, but it’s also where people can get themselves into trouble.

Sezzle is built to reduce friction at checkout. Instead of seeing one full price, you see the option to divide that total into smaller payments. Psychologically, that can make a purchase feel lighter.

And sometimes that’s genuinely helpful. If the purchase is planned and the payments fit comfortably into your budget, splitting it up may be a smart move.

But smaller payments can also make spending feel less serious than it really is.

That’s the part I think people should pay attention to. Sezzle doesn’t change what something costs. It changes when you pay for it.

How Sezzle Differs From a Credit Card

This is one of the most common misunderstandings. While both let you buy now and pay later, they’re structured very differently.

Credit Card

- Works as a revolving line of credit

- Can be used repeatedly without a fixed end date

- Allows you to carry a balance over time

- Often charges interest on unpaid balances

Sezzle

- Tied to a specific purchase

- Comes with a set payment schedule

- Breaks one transaction into fixed installments

- Often offers short-term interest-free options

That difference matters.

A credit card can turn into ongoing debt if balances are carried month to month. Sezzle can still cause issues if overused, but each purchase is usually contained within its own payment plan. That doesn’t make one better than the other. They’re just built for different types of spending.

Where Sezzle Fits Best

Sezzle tends to make the most sense for shoppers who want a little more flexibility without committing to a traditional credit product for every purchase.

It may work best when:

- The purchase is planned

- The payment schedule is easy to track

- The shopper knows the terms ahead of time

- The installments fit into the real budget, not the imagined one

That last point matters.

I think Sezzle is most useful when it supports a budget, not when it replaces one.

A Few Things Worth Watching

Even if Sezzle is easy to use, that doesn’t mean it should be used casually.

Before choosing it at checkout, it’s smart to pay attention to:

- Payment dates

- Any fees or extra costs

- The type of Sezzle product being offered

- How many other payment plans you already have active

This is where people often get tripped up. One installment plan may feel manageable. Three or four at the same time can feel very different. That doesn’t mean Sezzle is a bad option. It just means the convenience can make it easier to overcommit if you stop tracking the bigger picture.

The Bottom Line

Sezzle is a buy now, pay later service that lets shoppers split eligible purchases into smaller payments over time instead of paying the full amount upfront.

That makes it appealing for people who want more flexibility at checkout. It is not the same as a credit card, and it is not a free pass to ignore your budget. Like most financial tools, it can be useful when the purchase is planned, the payment schedule is clear, and the terms make sense.

If you think Sezzle is right for you, download the Sezzle app and see how easy it is to use.

FAQs

Sezzle is used to split eligible purchases into smaller payments over time instead of paying the full total upfront at checkout.

No, Sezzle is not the same as a traditional credit card. It is generally tied to individual purchases and structured payment plans rather than a revolving balance.

Most people use Sezzle for payment flexibility. It can make a purchase feel more manageable by spreading the cost across smaller installments.

It can, if the payment schedule fits comfortably within your budget. But it can also create problems if you take on more installment plans than you can realistically manage.

Sezzle is commonly associated with online checkout, though availability can depend on where the merchant offers it as a payment option.