50% of American adults used at least one BNPL service, and Affirm is one of the most popular…

But that doesn’t necessarily make it the best choice.

No buy now, pay later app is one-size-fits-all. So, if you’re looking for apps like Affirm that are a better fit for you, I’ve compiled a quick overview of the key options worth considering.

Here’s how I’d compare the main BNPL alternatives before making a decision.

Key Takeaways

- Compare Repayment Options: Apps like Affirm offer different payment plans, so flexibility can be a major factor when choosing.

- Klarna Offers Broad Flexibility: Klarna stands out for flexible plans and wide merchant availability across many markets.

- Afterpay Keeps It Simple: Afterpay is a strong pick for interest-free pay-in-four purchases and easy budgeting.

- Zip Has Wide Reach: Zip supports BNPL purchases online and in stores at millions of locations.

- Sezzle Adds Credit-Building Potential: Sezzle offers interest-free payments and optional credit-building through Sezzle Up.

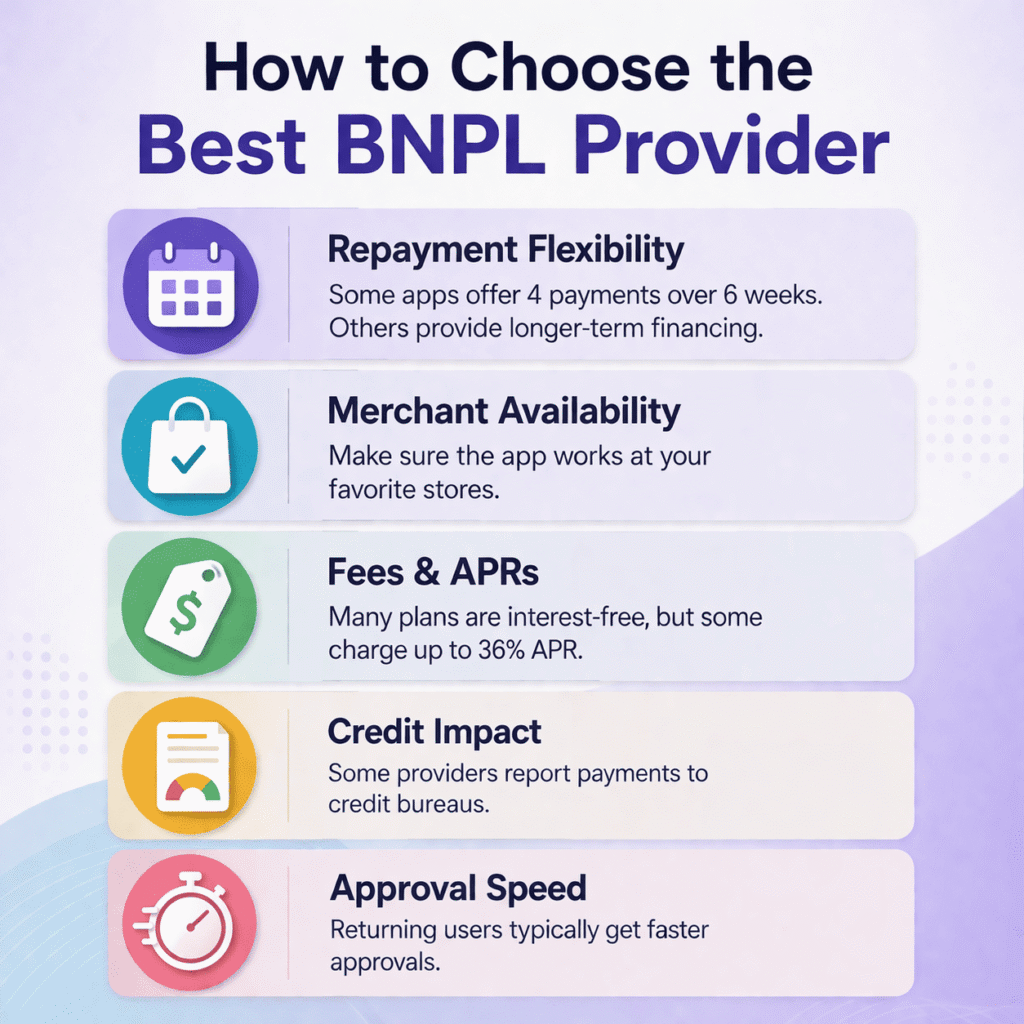

What To Look For In Apps Like Affirm Before You Choose One

When I compare apps like Affirm, I don’t just look at the brand name. I look at how the payments actually work in real life.

A few things matter most:

- Repayment flexibility: Some apps split purchases into 4 payments over 6 weeks. Others offer longer financing.

- Merchant availability: An app isn’t much help if your favorite stores don’t accept it.

- Fees and APRs: Some plans are interest-free, while others can charge APRs up to 36%.

- Credit impact: Some providers may report payments to credit bureaus.

- Approval speed: Existing users often get faster decisions.

I’d also check late-fee rules and whether the app works online and in stores—to see how well it fits into your actual lifestyle.

Sezzle: Best For Budget-Conscious Buyers Building Payment Flexibility

Sezzle is usually one of the first options I’d mention for shoppers who want a little more breathing room without overcomplicating things. I use it pretty frequently myself and love that it helps me manage my cash flow. It makes my finances feel simpler, more predictable, flexible, and overall. Just easier to stay on top of. Plus, it’s 100% app-based, so I never had to log in from a laptop just to see my balance.

Its standard plan splits purchases into four interest-free payments over six weeks. It’s also known for being more accessible to people with bad credit or limited credit history. Another big plus is Sezzle Up, which can help users build payment history through reported payments. And if you’d rather not have that activity reported, you can simply skip the program and use Sezzle on its own.

I never want to say that one option is the perfect fit for every BNPL user, because situations can vary a lot from person to person. That said, for budget-conscious folks who value something adaptive and modern that features straightforward payments and a chance to build better financial habits, I think Sezzle stands out in a really appealing way.

Klarna: Best For Flexible Payment Plans And Broad Retail Availability

Klarna is one of the more common Affirm alternatives, mostly because it gives shoppers a few different ways to pay. Depending on the purchase, that can include pay in 4 or longer-term financing.

The main thing I’d point to here is flexibility. If you want more than one payment option, Klarna usually gives you a bit more choice than some other apps. It’s also available at a wide range of retailers and works with major e-commerce platforms like Shopify and BigCommerce, which helps explain why it shows up so often at checkout.

If you shop across a lot of online stores and want a payment app with broad availability, Klarna makes sense. Just make sure you look at the terms before choosing a plan.

Afterpay: Best For Simple Pay-In-Four Purchases

Afterpay keeps things pretty easy, which is part of its appeal. The basic setup is simple: 4 interest-free payments spread over 6 weeks.

I think that works well for shoppers who don’t want to mess with too many choices. You buy the item, split the cost, and move on with your day.

Afterpay also has online and in-store shopping plus app deals, which can be useful if you already know where you want to shop. And if you pay on time, there’s no interest on the standard pay-in-four setup. For straightforward BNPL use, it’s a solid choice.

Zip: Best For Shoppers Who Want Widespread Merchant Coverage

Zip stands out mostly for how widely it can be used. If merchant coverage is your main concern, it’s one of the more practical alternatives to look at.

The app-based setup also works for both online and in-store purchases, which adds convenience. If your top priority is access rather than lots of plan variations, Zip makes a practical alternative.

Zip is another app like Affirm that’s worth a look, especially if merchant coverage is your main concern. It lets users split purchases into 4 payments over 6 weeks and can be used at millions of stores.

PayPal Pay Later And Splitit: Best For Checkout Convenience And Card-Based Installments

These two work a little differently from the other BNPL apps, so I like grouping them together.

PayPal Pay Later, including Pay in 4, is great for convenience. If you already use PayPal, approval can be fast, and initial checks may not affect your credit. That makes it a pretty painless option at checkout.

Splitit takes another route. Instead of creating a new loan, it uses your existing credit card and breaks the charge into installments. There’s no new credit check for that setup.

To me, PayPal is better for familiar checkout speed, while Splitit makes more sense if you want to use the card you already have.

Final Verdict

If you’re comparing apps like Affirm, the best choice usually comes down to what matters most to you.

Some are better for flexibility, some keep things simpler, and some are just easier to use at more stores.

I’d still look at Sezzle first. Whatever you choose, remember that the goal isn’t to find the pick with the biggest marketing budget; it’s to find the app that makes your life easier.

Frequently Asked Questions

Sezzle stands out for flexible payment options, offering pay-in-4 and longer-term financing, making it great for shoppers who want choices and in-store purchase functionality.

Afterpay offers a simple pay-in-4 interest-free plan over 6 weeks with no fees if paid on time, while Sezzle also provides 4 interest-free payments. However, Sezzle is often more lenient in accommodating bad or no credit.

Yes, most top BNPL apps work for both online and in-store purchases, giving you flexibility across millions of merchants.

Sometimes. Sezzle reports payments to credit bureaus to help build credit history if you opt in to the Sezzle Up program, while PayPal Pay Later often performs soft checks with no immediate credit impact. Always check each app’s policy before using.

Look at repayment flexibility, merchant acceptance, fees and APRs, credit impact, approval speed, and ability to use the app both online and in stores to find the best fit for your shopping habits.