The buy now, pay later industry is expected to quintuple from now to 2034.

Meanwhile, credit card debt stands at $1.28 trillion in the United States. But with the demonization and the list of talking points right now, it’s difficult to know which is better to use—if either.

As both a BNPL and a credit card user, I do feel they’ve both improved my life—but not everyone is talking about the smartest ways to use them.

In this guide, I’ll compare the two to help you decide which, if either, makes the most sense for your finances.

Key Takeaways

- Structure Changes Everything: BNPL usually feels easier to manage because the payments are fixed and the payoff date is clear, while credit card balances can stick around much longer.

- Flexibility Comes With More Temptation: Credit cards are more useful for everyday spending and emergencies, but that same flexibility can make overspending easier.

- Credit Building Usually Favors Cards: Credit cards are still the more reliable tool for building credit history, while most short-term BNPL plans are not broadly reported the same way (save for credit-history-building programs like Sezzle Up).

- BNPL Still Has Real Risk: Missing BNPL payments can lead to fees, collections, and possible credit damage, even if the plan looked harmless at checkout.

- The Best Choice Depends On The Purchase: BNPL often fits planned, short-term purchases better, while credit cards make more sense for ongoing spending and wider financial flexibility.

Quick Overview

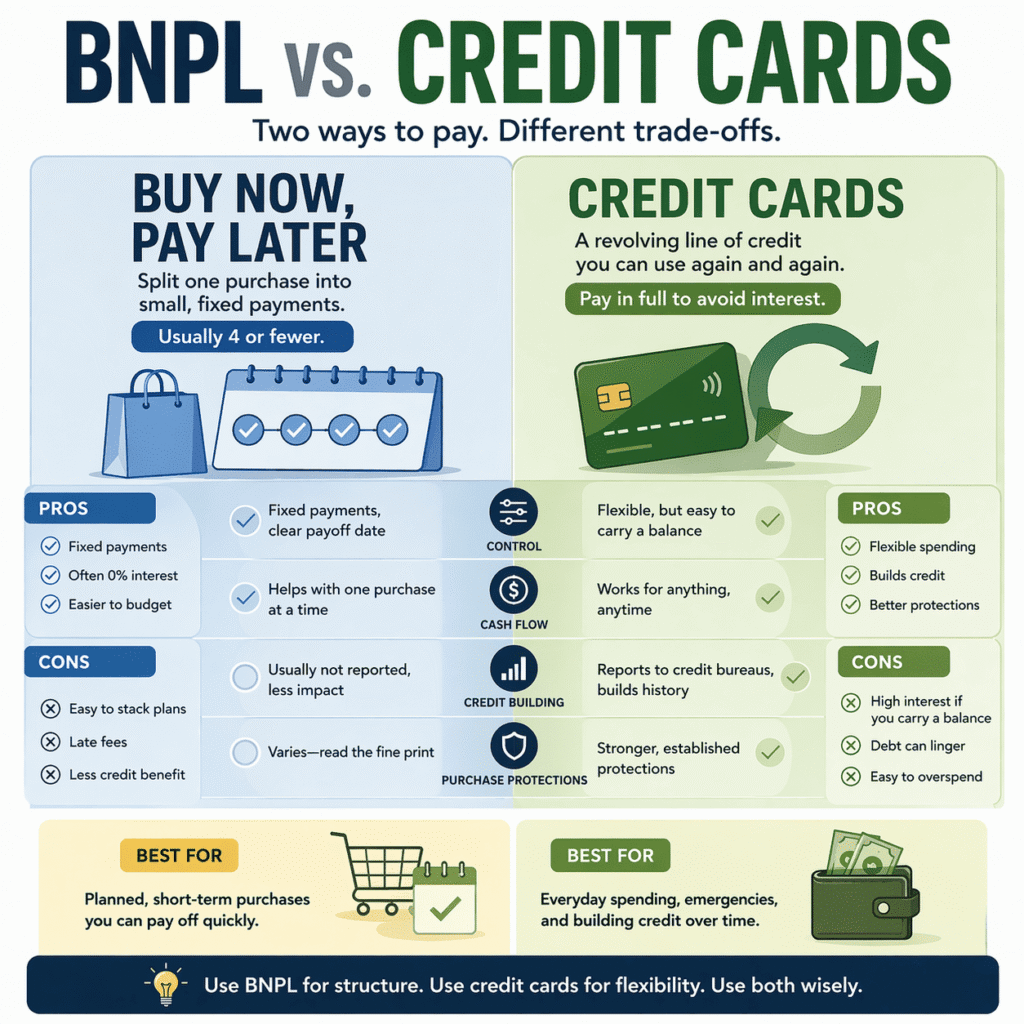

- Buy Now, Pay Later: Usually splits one purchase into a small number of installments, often four or fewer. Many short-term plans don’t charge interest, but missed payments can trigger late fees. It can give the opportunity to pay over time without paying more.

- Credit Cards: Give you a revolving line of credit you can reuse. They’re more flexible than BNPL, and if you pay the full statement balance on time, you can usually avoid interest. If you carry a balance, though, the cost can grow fast.

The Comparisons That Actually Matter

Which is easier to control?

This is where I give BNPL the edge. A fixed series of payments is easier for many people to manage than an open-ended credit card balance. With BNPL, you usually know the amount, the due dates, and the finish line right away. That structure can make it easier to decide whether the purchase truly fits your budget.

When I create a BNPL plan, I usually do the highest and quickest repayment with the lowest interest. This way, I require myself (upfront) to pay these debts off quickly.

Credit cards give you more freedom, but freedom is not always your friend at checkout. Because the balance can roll from month to month, it’s easier to underestimate the real cost of a purchase. Minimum payments keep the account current, but they can stretch repayment out and increase the total amount you pay.

Which is better for cash flow?

Honestly, both can help.

BNPL helps by breaking one purchase into smaller chunks. Credit cards help by giving you room to cover expenses now and pay by the statement due date. In practice, both can smooth out your budget when timing is tight. The difference is that BNPL is usually tied to one plan per item, while a credit card is a broader tool you can keep using for groceries, bills, travel, or emergencies.

So if your goal is structure, BNPL usually feels cleaner. If your goal is flexibility, credit cards win.

Which is better for building credit?

Credit cards are the clear winner here.

The CFPB explains that your credit report includes your credit activity, payment history, and the status of your credit accounts. Positive payment history on a credit card can help build and maintain a strong credit score over time. BNPL is more complicated. The CFPB has said BNPL reporting has historically been less consistent, and these loans have often not appeared in credit records in large enough volumes to work like traditional credit products.

That doesn’t mean BNPL never affects credit—especially if you enroll in programs designed to build your credit history, like Sezzle Up.

Which gives you stronger purchase protections?

Credit cards still have the more established dispute process, but BNPL providers can offer helpful protections too.

With a credit card, federal law gives you a clear billing-error process and familiar charge-dispute rights. BNPL works a little differently, so the exact refund and dispute steps can vary by provider, merchant, and payment plan. Still, many BNPL services offer ways to report issues, pause payments during review, or help coordinate refunds when something goes wrong.

That makes BNPL a useful option as long as you know the terms before checkout. The smart move is to check how refunds, returns, and disputes are handled so you can use the payment plan with more confidence.

BNPL vs Credit Card Comparison

| BNPL | Credit Cards |

|---|---|

| ✅ Fixed payments | ✅ Flexible spending |

| ✅ Easier to budget | ✅ Builds credit |

| ✅ Often no interest | ✅ Better protections |

| ❌ Easy to stack plans | ❌ Interest can be high |

| ❌ Late fees | ❌ Debt can linger |

| ❌ Less credit-building value | ❌ Easier to overspend |

The Biggest Risks to Remember

BNPL Risks

The biggest BNPL risk is that small payments can add up quickly. One plan may fit comfortably, but several open plans at once can make your budget harder to track. CFPB research has found that many BNPL users carry multiple loans at the same time, which is where due dates can start to pile up. Late fees or collections risk can add more pressure, so it’s worth keeping the full payment schedule in view before opening another plan.

Credit Card Risks

The biggest credit card problem is drag. The balance doesn’t always feel urgent because you can keep rolling it forward. That’s why interest becomes such a problem. You may stay current, make the minimum, and still spend months digging out of a purchase you barely remember making. For a lot of people, that open-ended timeline is the real danger.

How to Use Either Safely

A few habits matter more than the logo on the payment button:

- Check the total cost, not just the size of the next payment.

- Keep the number of open BNPL plans low so your due dates are easy to track.

- With credit cards, aim to pay the full statement balance on time whenever you can. That’s the cleanest way to avoid interest.

- Read the fine print on fees, refunds, and what happens if you miss a payment.

- Use either option for purchases that fit your budget already, not as a way to talk yourself into spending more. That last part is an inference, but it follows directly from how installment payments, interest, and multiple obligations can build up over time.

Final Verdict

If you want the simplest version, here it is: BNPL is often a strong choice for planned purchases because it gives you structure from the start. The payment schedule is usually clear, the payoff timeline is built in, and you’re not rolling the purchase into an open-ended balance.

Credit cards are usually better for flexibility, everyday spending, rewards, and long-term credit building. But for a specific purchase you already planned to make, BNPL can feel cleaner and easier to manage.

So the better choice depends on what you need most. If you want predictable payments and a set end date, BNPL may be the better fit. If you want broader flexibility and long-term credit value, a credit card may make more sense. Either way, know the rules before checkout so the payment method works for you.

FAQs

No. BNPL can be easier to budget for one planned purchase, but credit cards are usually more flexible and more useful for building credit history over time.

It can. The CFPB says most pay-in-four BNPL loans do not usually report positive payment history to the major credit bureaus, but missed payments that go to collections can hurt your credit scores.

No. If you pay your full statement balance on time, you can usually avoid interest, but carrying a balance can make the cost grow fast.

For many people, BNPL is easier to track because the payments are fixed and the end date is built in. Credit cards offer more flexibility, but that can make balances easier to carry for longer than expected.

Look at the payment schedule, total cost, possible fees, and whether the account could affect your credit. Those details matter more than the checkout pitch.