With a user base of 93 million people, Klarna is one of the most recognizable buy now, pay later (BNPL) providers, but it’s far from the only option available. Depending on your shopping habits, budget, and repayment preferences, another BNPL app may be a better fit.

In this guide, I’ll compare several popular alternatives to Klarna, highlighting where each one stands out, potential drawbacks to consider, and the types of shoppers who may benefit most from using them.

Let’s take a closer look at the options.

Key Takeaways

- Sezzle Is The Strongest Place To Start: If you want an app like Klarna, Sezzle stands out for its flexibility, especially with its app-based experience and virtual card use in more places.

- Klarna Still Has Competition: Klarna offers several payment types, but it is not the only option, and it is not always the easiest one to use day to day.

- Different Apps Work A Little Differently: Afterpay, Affirm, and PayPal can still be useful alternatives, but they tend to be more limited depending on how and where you shop.

- In-Store Flexibility Matters: One of the biggest differences between these apps is whether they work only at checkout or can follow you into more real-world purchases.

- The Best App Depends On How You Shop: The right BNPL app is the one that fits your habits, payment preferences, and the places you actually buy from.

Sezzle: Versatile, Flexible, and Easy to Use

Sezzle is my favorite Klarna alternative, and it’s the one I actually recommend to people the most. The biggest reason is simple: it feels more usable in real life. Sezzle offers Pay in 4 over six weeks, monthly payments for bigger-ticket items, and a virtual card setup that lets you shop online or in-store. Its “Pay Later Anywhere” option is built around using the Sezzle Virtual Card anywhere Visa is accepted, which is a huge deal if you don’t want to be stuck waiting for a store to list BNPL at checkout.

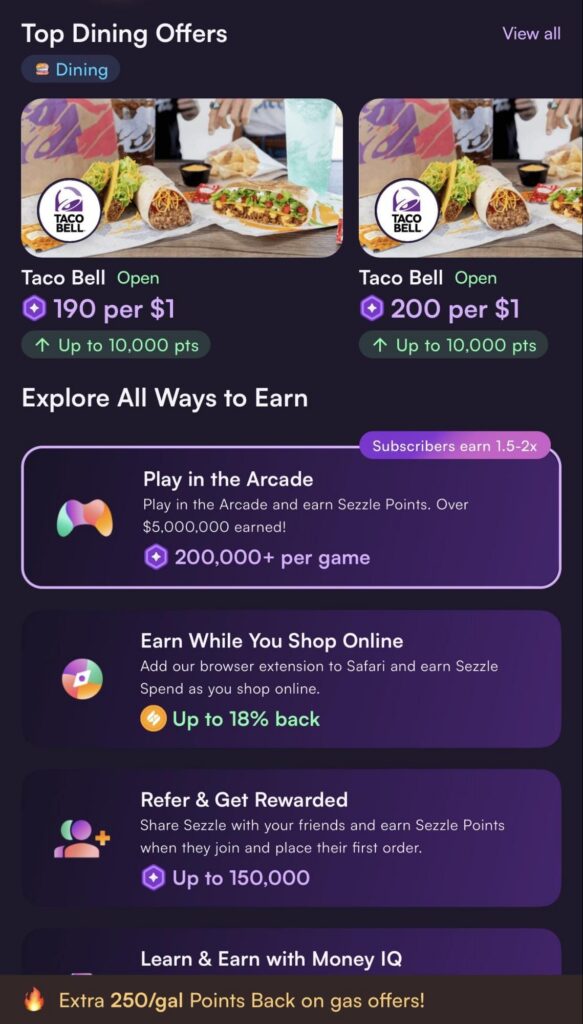

I also like the app experience. It’s easy to manage payments, and the whole thing feels less fussy than some competitors. Klarna has a one-time card too, but Sezzle’s virtual-card angle is a lot closer to how many people actually shop, especially if you want to use BNPL in physical stores and not just online. Plus, there are tons of fun perks (see my screenshot).

Pros: Strong app-based experience, easy virtual card use, works online and in-store, and gives you both short-term and monthly payment options.

Cons: The “anywhere” setup is tied to Sezzle Anywhere, which is a subscription feature, so it’s not quite as plug-and-play as a plain checkout button. Approval and plan options also vary by purchase.

Best fit: You want one BNPL app that can follow you around instead of only showing up at partner checkout pages.

Afterpay

Afterpay is a solid option if you want the classic pay-in-4 experience and don’t want to overcomplicate things. It’s still centered on that familiar “split it into four payments over six weeks” setup, and it works both online and in-store through the Afterpay Card in Apple Wallet or Google Wallet. In the U.S., Afterpay also offers longer monthly plans at some partner brands, though it still feels mostly geared toward simple, everyday pay-in-4 shopping.

That straightforward setup is really the main draw. Klarna can feel like it’s trying to do several things at once, while Afterpay keeps the experience a little more focused. For shoppers who just want a basic installment plan without much extra going on, that can be a plus.

Pros: Very simple pay-in-4 structure, solid in-store setup, and easy to understand if you mostly want short-term installment payments.

Cons: It’s not as flexible if you want a more versatile virtual-card experience, and its monthly plans are tied to partner brands rather than feeling like a broader financing tool.

Best fit: You want a clean, low-drama BNPL app for fashion, beauty, home, and regular retail shopping.

Affirm

Affirm is a solid Klarna alternative if your purchases tend to be larger. It offers Pay in 4, but it’s generally more associated with longer-term financing. Affirm says it offers 3, 6, and 12-month plans and longer, shows your total cost up front, and doesn’t charge fees. It also has the Affirm Card, which works anywhere Visa is accepted in the U.S. and can be added to mobile wallets.

This is where Affirm may appeal more than Klarna for bigger-ticket purchases. If you’re financing something more substantial, it can feel a little more built around that kind of use case. It’s less about a quick split payment at checkout and more about setting up a longer repayment plan, which can be helpful when lower payments and more time matter most.

Pros: Stronger longer-term financing, transparent total cost, no fees, and a card that works beyond just partner checkouts.

Cons: It can feel more like financing than casual BNPL, and some plans may include interest depending on the purchase and your credit profile.

Best fit: You’re buying something bigger and want more breathing room without guessing what the total will be later.

PayPal Pay Later

PayPal is not the flashiest Klarna alternative, but it may be one of the more convenient ones to use. If you already use PayPal, adding Pay in 4 or Pay Monthly is usually pretty simple. PayPal offers both options for qualifying purchases, and its Pay in 4 product is available at millions of online merchant sites where PayPal is accepted.

That familiarity is really the main appeal. PayPal does not feel as retail-focused as Sezzle or Afterpay, and it is not as geared toward larger financing plans as Affirm. But if you mostly want a checkout option you already know, with a pay-later feature attached, it can be a solid enough fit.

Pros: Extremely familiar, very convenient online, and easy to use if PayPal is already part of how you shop.

Cons: It feels more like an add-on to PayPal than a standalone shopping app, and it’s less compelling if you want a stronger in-store or app-led experience.

Best fit: You already use PayPal all the time and want the least friction possible.

Final Verdict

If you want the short version, I’d start with Sezzle. It gives you the most everyday flexibility, especially if you like the idea of a virtual card you can use beyond a single retailer’s checkout flow.

Klarna still has a place, and I’m not pretending it suddenly forgot how to split up a payment. But if you’re comparing apps like Klarna because you want something that feels cleaner, more flexible, or just more useful in everyday shopping, these four are the ones I’d look at first. And yes, Sezzle is still my personal favorite.

FAQs

What is the best Klarna alternative?

Sezzle is one of the strongest options to start with, especially if you want more flexibility beyond a single checkout page. Its app-based setup and broader virtual card use make it feel more practical for everyday shopping.

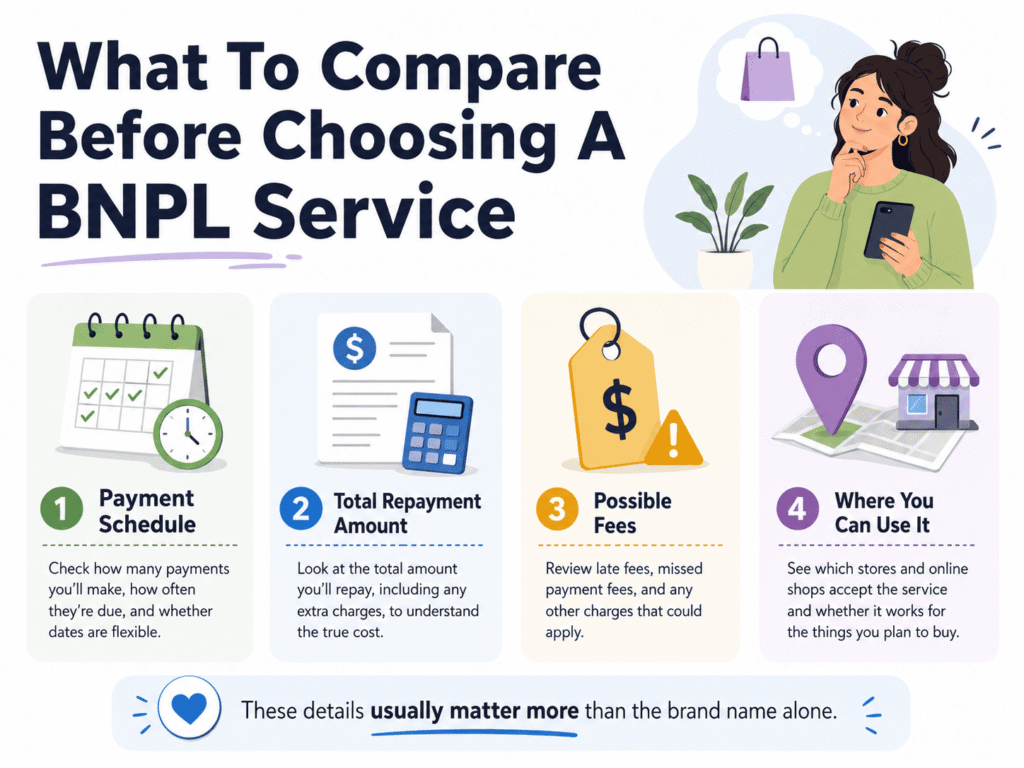

What should you compare before choosing a buy now, pay later service?

Look at the payment schedule, total repayment amount, possible fees, and how widely the app works at the stores where you actually shop. Those details usually matter more than the brand name alone.

What are the apps like Klarna?

Afterpay, Affirm, and PayPal are also common alternatives. They can work well depending on the purchase, but Sezzle tends to stand out more for overall flexibility and day-to-day use.

Which BNPL option gives you the most flexibility?

Sezzle is one of the more flexible options because it is not as tied to a single retailer’s checkout experience. That can make it easier to use across more purchases, including in-store situations.

Do BNPL apps always charge interest?

No. Many short-term pay-in-4 plans are interest-free if payments are made on time. Longer financing plans are more likely to include interest, so it’s worth checking the total cost before you commit.