I’ve compared quite a few BNPL providers…

But few comparisons have shocked me as much as this one.

Sezzle vs. Credova is tricky because they’re apples and oranges, polar opposites—broad vs. niche, flexible vs. firm, and easy vs. complex.

After diving headfirst into both services, here’s your definitive guide to making the right decision for your next buy now, pay later purchase.

Which Provider to Choose:

- If you want everyday flexibility, Sezzle’s short-term plans make it easier to split practical purchases without turning them into a long financing commitment.

- If you want a cleaner app experience, Sezzle gives you a smoother way to track due dates, payments, and upcoming balances without much clutter.

- If you want more places to use BNPL, Sezzle Anywhere can make the platform feel more useful beyond standard partner checkouts.

- If you want optional credit-building, Sezzle Up gives responsible users a way to have their payment history reported without forcing that feature on everyone.

- If you already shop with Credova’s specialty retail partners, Credova may work if you know the exact merchant, understand the terms, and plan to pay the balance off quickly.

Comparison Table

| Category | Sezzle | Credova |

|---|---|---|

| Best For | Everyday purchases, cash-flow smoothing, short-term payment control | Specialty retail financing through specific merchants |

| Payment Options | Pay in 2, Pay in 4, Pay in 5, Pay in Full, and some monthly financing | Lease-to-own or installment loan options, depending on the merchant and product |

| Main Strength | Simple, flexible short-term payments with a useful app experience | Can finance larger purchases at select specialty retailers |

| Fees + Interest | It’s usually minimal when managed carefully, but fees and subscriptions can apply | Can become costly if terms, timing, or payoff windows are misunderstood |

| App Experience | Clean, calm, and easy to track | No strong dedicated app |

| Special Programs | Sezzle Up, Anywhere, virtual card access, optional credit reporting | More focused on merchant-based financing than broader financial tools |

Sezzle vs. Credova Overview

Sezzle: Day-to-Day Ease

Sezzle is a buy-now, pay-later app built around short-term payment control. Its main appeal is that it lets you split purchases into clear payment plans like Pay in 2, Pay in 4, or Pay in 5, while also offering Pay in Full and monthly financing on some purchases.

The app is helpful for covering daily expenses, surprise bills, or things you need right away, but would rather not charge to a credit card. It offers extra features like Sezzle Up and Anywhere, so it does more than a basic buy now, pay later tool. Overall, it’s a good choice if you want flexibility and an easy-to-use experience.

Pros

✅ Clear Payment Structure: Sezzle’s short-term plans are easy to understand, which makes it easier to know exactly what you owe and when.

✅ Useful Everyday Flexibility: Sezzle Anywhere and the virtual card make it feel more practical beyond a limited partner checkout network.

✅ Calm App Experience: The app makes it easy to see upcoming payments, completed payments, and what is due next without feeling overwhelmed.

✅ Optional Credit Building: Sezzle Up gives responsible users a way to have payment history reported without forcing that feature on everyone.

Cons

❌ Fees Can Add Up: Service fees, late fees, failed-payment fees, reschedule fees, and other charges can matter if you are not careful.

❌ Best Features May Require Membership: The most flexible version of Sezzle can involve subscriptions or added costs.

❌ Still Requires Discipline: It works best when you already know the purchase is manageable and you stay organized with due dates.

Credova: Specialized, Niche Purchases

Credova is a more specialized financing platform that feels less like a casual BNPL app and more like merchant-based financing. It is commonly tied to specific retailers in categories like outdoor gear, tactical stores, workwear, farming, ranching, and other specialty shopping areas.

Instead of giving you broad flexibility to use an approval almost anywhere, Credova tends to connect the financing to a particular merchant. Depending on the purchase, the agreement may be structured as a lease-to-own arrangement or an installment loan. That makes it better suited for shoppers who already know the store, understand the terms, and plan to pay close attention before agreeing.

Pros

✅ Useful for Specialty Retailers: Credova can make sense when you are already buying from a specific partner merchant.

✅ Potential For Larger Purchases: The platform may offer approvals that fit bigger-ticket purchases better than a small pay-in-4 plan.

✅ Early Payoff May Help: Some agreements may be more manageable if you understand the payoff window and clear the balance quickly.

✅ Targeted Financing Option: For shoppers already comfortable with its merchant network, it can serve as a focused store-financing tool.

Cons

❌ Merchant-Locked Experience: The approval can feel tied to one retailer, which limits flexibility compared with a broader BNPL app.

❌ Terms Can Feel Murky: Lease-to-own versus installment loan structures can make the real cost harder to judge quickly.

❌ Account Experience Feels Weak: The lack of a smooth app or easy portal experience can make the whole process feel less reassuring.

❌ No Dedicated App: Unlike with Sezzle, there is no dedicated app for Credova.

Payment Flexibility

Sezzle feels much more natural as an everyday payment tool. I like that its short-term plans are easy to picture before using them. If I split a $200 purchase into four payments, I know I am dealing with four $50 payments, and that clarity makes the decision feel lighter.

The real strength is that Sezzle does not feel like a major financing event. It feels like a way to smooth out timing when the purchase already makes sense. Sezzle Anywhere also adds a lot here because the virtual card makes the app more useful online and in stores where Visa is accepted, with some exceptions.

Credova is much less flexible in the way I think about BNPL flexibility. It feels tied to the merchant first, not the shopper first. Once you pick a retailer, the experience can feel locked into that store, which is very different from opening an app and choosing how to manage a purchase across a wider range of situations.

I get why it makes sense if you already know which store and item you want, but I don’t like how fast it goes from browsing to approval and then straight to the merchant. It feels less like having financial flexibility and more like being rushed down a single path.

Winner: Sezzle. It gives you more practical, everyday flexibility without making the process feel overly committed too early.

Fees, Interest, and Real Cost

Sezzle works well if you use it with intention, purpose, and care. The short-term payment plans are straightforward, especially if you stick to the schedule and avoid making changes.

However, you might still see fees depending on how your order is set up and how you manage your account. Service fees, failed-payment fees, late-payment fees, reschedule fees, and Late Saver fees can all affect your experience with the purchase.

I still like Sezzle overall, but it works best if you stay organized. It is helpful for people who keep track of due dates and don’t see split payments as free money.

Credova makes me more careful about costs because its structure can change a lot. Sometimes it is a lease-to-own agreement, other times it is an installment loan, so I always feel like I need to slow down and read all the details.

Paying off early might help if you know exactly what you are doing and plan to pay off the balance quickly, but that is also where the risk comes in. If you miss the timing or do not fully understand the agreement, the cost can end up being much higher than you expected. It feels more like old-fashioned specialty financing than a simple BNPL tool.

Winner: Sezzle. It still requires attention, but the cost structure feels easier to understand and manage.

App Experience and Account Access

Sezzle gives me the kind of app experience I want from a payment product. It feels calm, straightforward, and easy to use. I can quickly see what I owe, what I have already paid, and what is coming up, all without having to sort through clutter. This is more important than people realize, since the app is where you go to stay organized.

I do not want a payment app that pushes me to shop more every time I check a due date. Sezzle feels more like a budgeting tool than a flashy shopping feed, and I like that.

Credova did not give me the same sense of control. The experience feels more scattered, especially when you are trying to check your approval status, account details, merchant connection, or payment setup. Since is there is no app, everything is difficult.

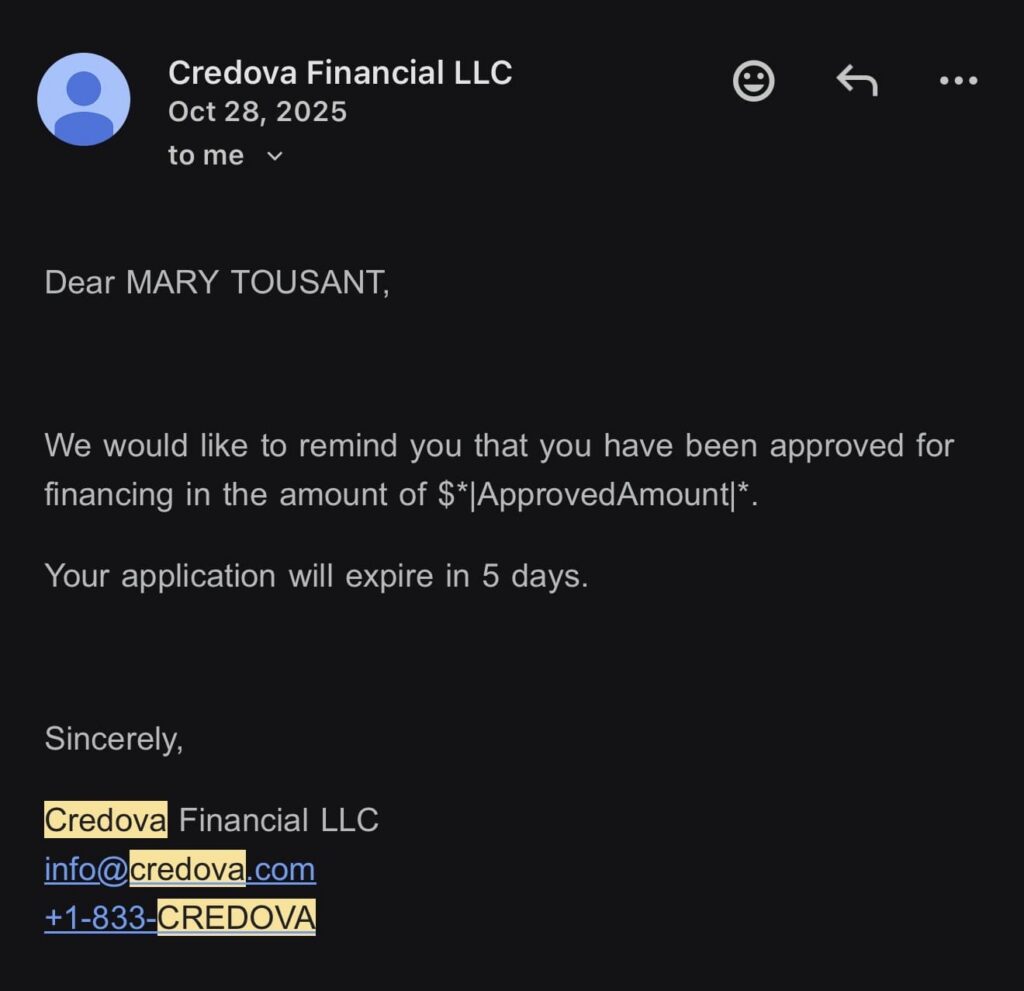

Because of this, I never even used Credova, although I did try to go through the approval process, but the system glitched. What’s even stranger is that for months, they continued to send me emails like the ones above that seemed autogenerated and in error since the amount was filler info.

Winner: Sezzle. The app feels easier to live with, easier to track, and much more reassuring than what Credova provides.

Extra Features, Memberships, and Credit Tools

Sezzle has a stronger set of extras, and I like that they do not all feel forced. Sezzle Up is probably the best example because the credit-building feature is optional. If I want my payment history reported, I can opt in, but if I only want to use Sezzle as a short-term payment tool, I can do that, too.

Sezzle Anywhere makes the platform more helpful for people who want more ways to use it, especially with the virtual card. Not everyone will need every upgrade, and some extra features cost money, but overall, the system seems designed for real users.

When I use a payment service, I want to know exactly who I am dealing with and where to get help. With Credova, this is not always obvious, so I would keep screenshots, save emails, write down payoff terms, and make sure I know who manages the account.

Winner: Sezzle. Its extras feel more useful, more optional, and better connected to how people actually manage payments.

Final Verdict

Sezzle is the better choice for most people. It’s simpler, more flexible, and easier to use day-to-day. I prefer it for situations where timing matters more than affordability. If you need to buy supplies, household items, event materials, or anything practical right away, Sezzle gives you some breathing room without turning your purchase into a long-term commitment.

Sezzle is the winner by a wide margin because it helps me feel in control of my payments. In comparison, Credova seems like a service worth treading carefully around.

FAQs

Is Sezzle better than Credova?

For most everyday shoppers, yes. Sezzle feels easier to understand, more flexible, and much smoother to manage than Credova.

What is the biggest difference between Sezzle and Credova?

Sezzle feels like a short-term BNPL app for regular purchases, while Credova feels more like merchant-based financing for specialty retailers.

Does Sezzle charge interest?

Sezzle’s short-term plans can be interest-free, but fees may still apply depending on the order, payment timing, reschedules, or account setup.

Why would someone use Credova instead of Sezzle?

Credova may make sense for someone buying from a specific partner merchant, especially in specialty retail categories, who understands the agreement and plans to pay quickly.

Which option is better for simple payment splitting?

Sezzle is the better fit for simple payment splitting because the plans are clearer, the app is easier to use, and the experience feels less contract-heavy.