Roughly 40% of Americans who use BNPL use it for apparel—and for good reason.

Whether you’re upgrading your wardrobe or replacing a beat-up pair of sneakers, buy now, pay later shoes allow you to spread the expense over time, giving you a handful of paychecks to work with instead of just your bank account balance.

But there are some tips and tricks to finding the best places to shop and doing it right.

I’ll take you through it: everything you need to know about BNPL shoes, and nothing you don’t.

Key Takeaways

- Timing Matters With Shoes: BNPL helps you buy when your size, sale price, or deadline still exists.

- Pay-In-4 Fits Most Shoe Purchases: Sneakers, work shoes, running shoes, and kids’ shoes often work well with short installment plans.

- The Right Pair Beats The Cheapest Pair: BNPL can make it easier to choose shoes that actually fit, last, and solve the problem.

- Returns Matter More With Shoes: A smooth exchange or refund process is essential because fit is never guaranteed.

- Monthly Payments Fit Bigger Carts: Designer shoes, premium boots, luxury sneakers, or family shoe hauls may need more flexible terms.

The Real Reason BNPL Works So Well For Shoes

Timing is a big issue when you’re buying shoes.

With some purchases, waiting a few weeks does not change much. With shoes, waiting can change everything.

- Your size sells out.

- The sale ends.

- The color you wanted disappears.

- Your kid outgrows their current pair before you planned for it.

- Your work shoes become uncomfortable enough that every shift feels longer.

- Your running shoes lose support before your budget is ready to replace them.

BNPL helps because it gives you a way to act when the pair is available, not only when the full price feels convenient.

That is especially useful because shoes sit in a strange spending category. They can be practical, emotional, urgent, style-driven, or all of those at once. A pair of slip-resistant work shoes is not the same kind of purchase as limited-release sneakers, but both can come with pressure. One is about comfort and safety. The other might be about availability and timing. In both cases, paying later can make the decision easier without forcing you to settle or wait.

Different Shoe Purchases Have Different Priorities

The best BNPL shoe purchase starts with the reason you are buying. Not all shoes solve the same problem, so the payment choice should fit the situation.

| Shoe Purchase | What Actually Matters | Why BNPL Helps |

|---|---|---|

| Work Shoes | Comfort, durability, and having them before your next shift | You can replace bad shoes before they become a daily problem |

| Kids’ Shoes | Sudden growth, school, sports, and buying more than one pair | You can handle the cart total without taking the full hit at once |

| Running Shoes | Support, cushioning, and avoiding pain from worn-out shoes | You can replace them when your feet need it, not weeks later |

| Sneakers | Size, colorway, release timing, and availability | You can grab the pair while it’s still in stock |

| Boots | Weather, quality, and seasonal timing | You can choose a better pair without absorbing the full cost upfront |

| Event Shoes | A specific date, outfit, or occasion | You can buy for the deadline instead of waiting until it’s inconvenient |

| Designer Shoes | Higher price, style, and limited availability | You can make a premium purchase easier to budget around |

This is the part many generic BNPL articles miss. The payment plan is not the whole story. The real value is that BNPL helps you buy the right pair at the right moment.

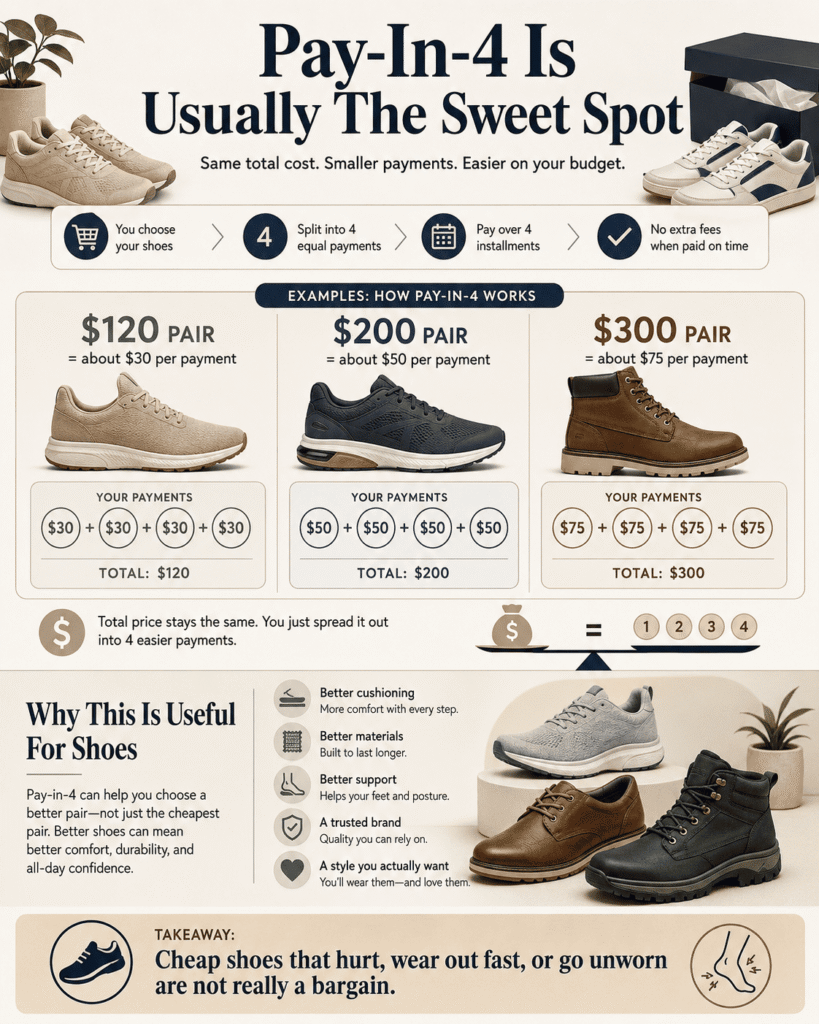

Pay-In-4 Is Usually The Sweet Spot

For most shoes, pay-in-4 is the easiest BNPL structure to understand. Instead of paying the full amount at checkout, the cost is split into four smaller payments.

A $120 pair becomes about $30 per payment. A $200 pair becomes about $50 per payment. A $300 pair becomes about $75 per payment.

That difference is important. The total price stays the same, but it feels different on your budget. Paying $200 at once can be tough, while $50 is easier to fit into your week.

This is where BNPL is especially favorable for shoe shopping. It lets you buy better without necessarily buying recklessly. Instead of choosing the cheapest pair because it is the easiest to pay for upfront, you can choose the pair that actually meets your needs: better cushioning, better materials, better support, a brand you trust, or the style you really wanted.

That can be the smarter decision. Cheap shoes that hurt, wear out quickly, or go unworn are not really a bargain.

The One Thing That Can Ruin A BNPL Shoe Purchase

The biggest risk with shoes is not the payment plan. It’s fit.

Shoes are personal in a way that many other products are not. A pair can look perfect online and still feel wrong the second you put it on. One brand runs narrow. Another runs large. A boot feels stiff. A sneaker rubs at the heel. A dress shoe looks great, but becomes unbearable after twenty minutes.

That’s why the store’s return and exchange policy is so important with BNPL. Even if the payment plan is easy, if the shoes don’t fit and returns are a hassle, the whole process can be frustrating.

So, a good BNPL shoe purchase should leave you with a clear path to exchange sizes, return the pair, or get a refund without confusion. This matters even more with clearance items, final-sale shoes, resale sneakers, and designer pairs, where return rules can be stricter.

When Monthly Payments Make More Sense

Pay-in-4 works well for everyday shoes, sneakers, work shoes, running shoes, and moderately priced boots. But monthly payments can make more sense when the total is higher or when you are buying more than one pair at once.

Monthly payments may be a better fit for:

- Designer shoes or luxury sneakers

- Premium boots with a higher upfront price

- Family shoe orders with multiple pairs

- Back-to-school shoe shopping

- Replacing several worn-out pairs at once

The goal is not to stretch every shoe purchase as long as possible. It’s to match the payment plan to the purchase. A short plan is usually better for a normal pair of shoes, while a longer plan may feel more comfortable for a higher-ticket order.

Bottom Line

You might need shoes for work, school, a trip, a race, a wedding, an interview, a season, or a limited release. If you wait until paying full price feels easy, you could miss out, lose your size, pay more later, or keep wearing shoes that need replacing.

BNPL gives you more control over that moment. You can buy when the shoes are available and useful, spreading the cost into easier-to-handle payments.

That is what makes buy now, pay later such a natural fit for shoes. It’s not just about spending less today; it’s about getting the right pair before the opportunity, deadline, or need passes.

Want one of my favorite BNPL options? Check out my experience with Sezzle and see if it’s for you.

FAQs

Can you buy shoes with buy now, pay later?

Yes. Many shoe retailers and BNPL providers let shoppers split purchases into smaller payments instead of paying the full price upfront.

Is BNPL good for buying shoes?

BNPL can be a strong fit for shoes because size, timing, and availability often matter. It helps you buy the pair you need or want without waiting until the full payment feels convenient.

What type of shoes work best with pay-in-4?

Pay-in-4 usually works well for sneakers, running shoes, kids’ shoes, work shoes, casual shoes, and moderate-price boots. The short payment schedule keeps the purchase simple.

What should I check before buying shoes with BNPL?

Check the return policy, exchange options, final-sale rules, payment dates, and what happens if you return the shoes before all payments are complete.

When do monthly payments make sense for shoes?

Monthly payments may make sense for designer shoes, premium boots, luxury sneakers, or larger carts with multiple pairs. They can make a higher total easier to manage over time.