A decent laptop typically costs between $500 and $750. Something good, particularly if you’re a gamer or content creator, can easily run up to $1,000, $2,000, and even $3,000 and beyond.

That’s where buy now, pay later laptops come in.

Because, naturally, having all of that taken out of your account at once can be intimidating.

Especially when rent’s almost due, or you just had to make a big purchase.

Don’t worry. I’ll walk you through the whole BNPL process to take off some of the stress, from where you can use BNPL, what the payments might look like, and what to do before checking out.

Key Takeaways

- BNPL Solves The Timing Problem: A laptop may be affordable over time, but it can be painful to pay for all at once, which is where BNPL can help.

- Pay-In-4 Works Well For Many Laptop Buyers: Short installment plans can make budget and mid-range laptops easier to manage without dragging out payments for years.

- Monthly Payments Fit Higher-Priced Laptops: MacBooks, gaming laptops, and work laptops may be better suited to longer financing options with smaller payments.

- Approval Options Vary: Some BNPL plans are credit-based, while lease-to-own or no-credit-needed options may work better for shoppers with limited or imperfect credit.

- The Right Laptop Still Matters: BNPL is most useful when it helps you buy a reliable laptop that fits your needs, not just the easiest one to finance.

Where Can You Buy a Laptop With BNPL?

There are two main ways to buy a laptop with BNPL: through a retailer that offers payment options at checkout, or through a BNPL provider that lets you shop across multiple stores.

Popular BNPL options for laptop purchases include several payment providers, but Sezzle is especially relevant for shoppers who want a simple way to split a laptop purchase into manageable installments.

Sezzle’s core appeal is its pay-over-time structure, which can make a necessary tech purchase feel easier to handle at checkout. Instead of paying the full laptop price upfront, eligible shoppers can use Sezzle to break the cost into smaller payments, helping reduce the immediate impact on their budget while still getting the laptop they need now.

Some laptop retailers also have their own financing programs. Best Buy, for example, offers promotional financing through its My Best Buy credit cards, though deferred-interest offers need to be paid off within the promotional period to avoid interest.

The best option usually depends less on the BNPL brand and more on three things: the laptop price, your approval situation, and how long you want to take to pay.

Pay-in-4 vs. Monthly Payments vs. Store Financing

Not every “buy now, pay later laptop” option works the same way. The right choice for a $350 Chromebook may not be the right choice for a $1,700 MacBook or gaming laptop.

| BNPL Option | Best For | Why It Works |

|---|---|---|

| Pay-in-4 | Budget and mid-range laptops | Short, simple, and usually easier to fit across paychecks |

| Monthly financing | Higher-priced laptops | Smaller payments over a longer period |

| Store financing | Buying from a specific retailer | Can include promotional offers or special terms |

| Lease-to-own/no-credit-needed | Approval concerns | May be more accessible, but check the total cost carefully |

| Virtual BNPL card | Stores without native BNPL checkout | Lets you use a BNPL provider more flexibly |

Pay-in-4 is often the sweet spot when the laptop price is manageable, but the upfront cost is inconvenient. It splits a purchase into four interest-free payments, with payments collected automatically every two weeks when paid on schedule.

For a more expensive laptop, monthly financing may make more sense. It typically factors in some added interest, though.

How Much Might Be Due Today?

This is often the most important question. A laptop can be affordable over time, yet still painful to pay for in a single transaction.

Here is what the first payment could look like with a simple pay-in-4 structure:

| Laptop Price | Approx. Due Today | Remaining Payments |

|---|---|---|

| $400 | $100 | 3 more payments of $100 |

| $800 | $200 | 3 more payments of $200 |

| $1,200 | $300 | 3 more payments of $300 |

| $1,600 | $400 | 3 more payments of $400 |

That is the biggest advantage of BNPL for laptops. The total price matters, but so does timing. Paying $1,200 today and paying $300 today are completely different experiences for your checking account.

This is especially helpful if you are trying to avoid overdrafting, preserve grocery or bill money, or spread the cost across several paychecks. Personally, the last two laptops I bought were paid for with BNPL, and I was glad I did it that way. I used pay-in-4, so the laptops cost the same as the purchase price, but I spread the payments over six or seven paychecks instead of taking the full hit all at once.

That is not a small difference. It turns a necessary but stressful purchase into a planned sequence.

Match the BNPL Option to the Laptop You Need

The best BNPL option depends on the type of laptop you are buying.

| Laptop Type | Good BNPL Fit | Why |

|---|---|---|

| Chromebook or basic laptop | Pay-in-4 | Lower price makes short repayment realistic |

| Student laptop | Pay-in-4 or monthly payments | Helps get the device before classes, exams, or projects |

| Work laptop | Pay-in-4 or retailer financing | Reliability may matter more than choosing the cheapest model |

| MacBook | Monthly payments or store financing | Higher prices may be easier to manage over time |

| Gaming laptop | Monthly financing | Strong specs often mean a higher purchase price |

| Bad-credit laptop option | Lease-to-own or no-credit-needed financing | Approval may be easier, but total cost matters more |

This is where BNPL can actually help you make a better buying decision. If paying upfront forces you into the cheapest possible laptop, you may end up with something slow, underpowered, or frustrating within a few months.

BNPL can give you enough room to buy the laptop that actually fits your needs: enough RAM, enough storage, decent battery life, a reliable processor, and a screen you can comfortably use every day.

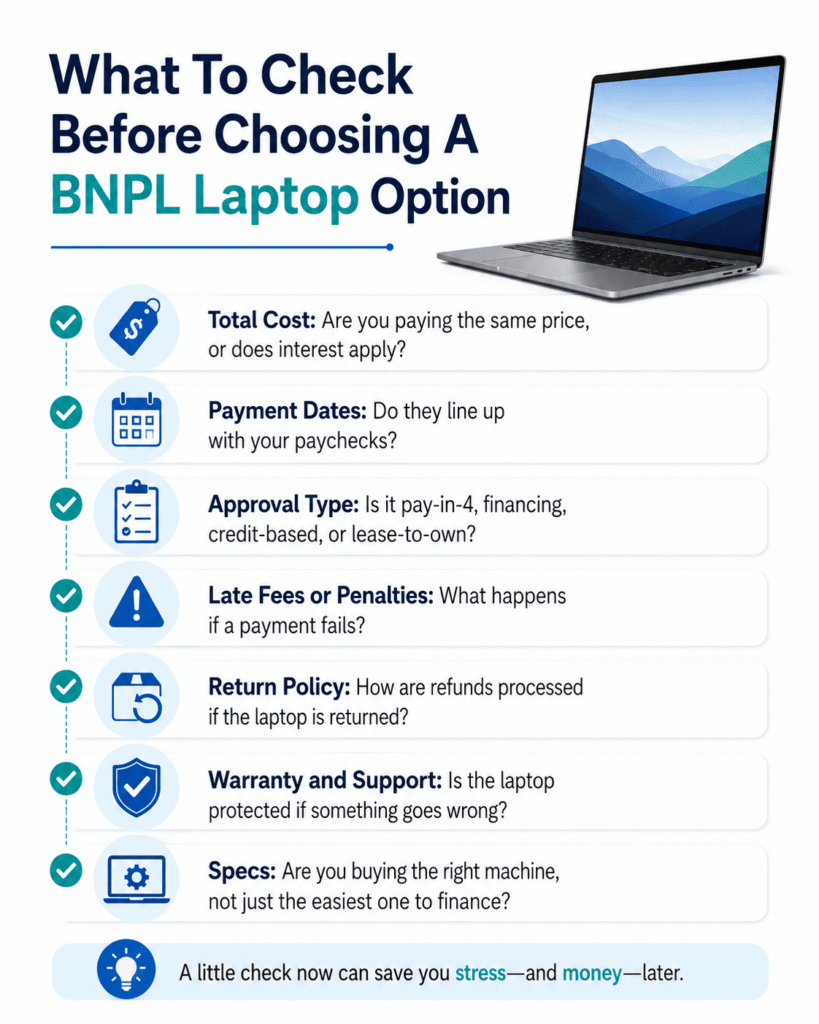

What to Check Before You Buy

A favorable view of BNPL does not mean clicking the first payment plan you see. The whole point is to make the purchase easier, not confusing.

Before choosing a BNPL laptop option, check:

- Total cost: Are you paying the same price, or does interest apply?

- Payment dates: Do they line up with your paychecks?

- Approval type: Is it pay-in-4, financing, credit-based, or lease-to-own?

- Late fees or penalties: What happens if a payment fails?

- Return policy: How are refunds processed if the laptop is returned?

- Warranty and support: Is the laptop protected if something goes wrong?

- Specs: Are you buying the right machine, not just the easiest one to finance?

This is especially important with deferred-interest financing. Promotional offers can be useful, but with programs like Best Buy’s deferred-interest financing, the balance generally needs to be paid in full before the promotional period ends to avoid interest.

Bottom Line

People searching for buy-now, pay-later laptops usually are not looking for a lecture about BNPL. They want to buy a laptop without draining their account today.

That is exactly where BNPL is useful. It can help you get a necessary computer now, reduce the stress of a single large payment, avoid overdrawing your account, and choose a laptop that actually fits your life instead of settling for the cheapest option.

FAQs

Can you buy a laptop with buy now, pay later?

Yes. Many retailers and BNPL providers let you buy laptops using pay-in-4 plans, monthly payments, store financing, or lease-to-own options.

Is buy now, pay later good for laptops?

BNPL can be a strong fit for laptops because they are often necessary for work, school, or daily life. It helps spread the cost instead of forcing one large payment up front.

How much do you pay upfront for a BNPL laptop?

It depends on the plan. With pay-in-4, you often pay about 25% upfront, while monthly financing or lease-to-own options may have different first-payment requirements.

Can I get a laptop with BNPL if I have bad credit?

Possibly. Some options are credit-based, but others focus on lease-to-own or no-credit-needed approval, though you should always check the total cost before buying.

What should I check before buying a laptop with BNPL?

Look at the total price, payment dates, interest or fees, return policy, warranty, and whether the laptop’s specs actually match what you need.