Jewelry is expensive—$500 spent a year on average—and pretending otherwise doesn’t help anyone.

But jewelry is also part of our lives. It can help us look presentable, feel confident, express ourselves—and of course, it can be an eternal statement of love.

But a decent necklace, ring, bracelet, or pair of earrings can easily cost more than you planned to spend that week. That doesn’t always mean the purchase is irresponsible. Sometimes it just means the timing is awkward.

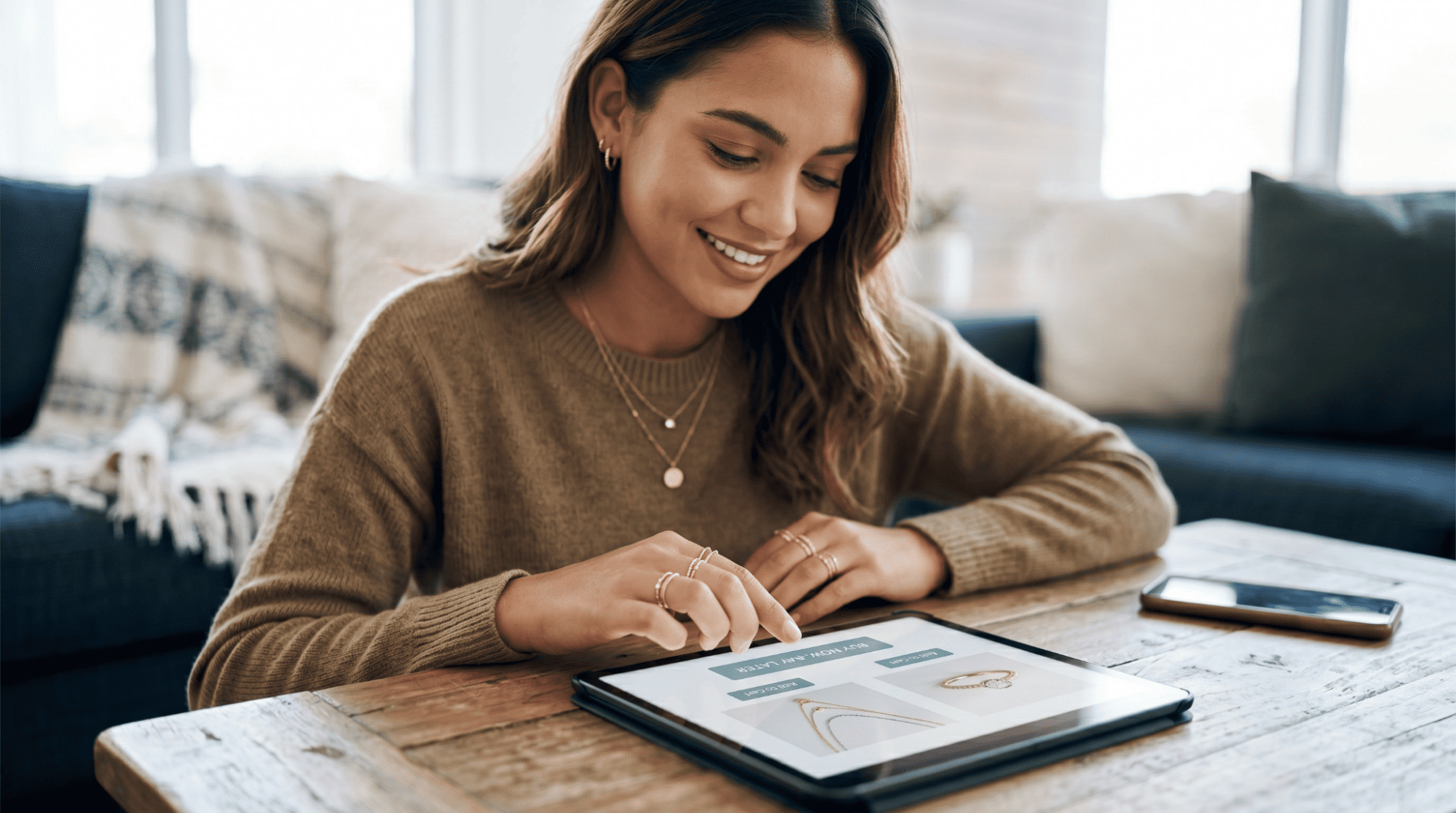

That’s where buy now, pay later jewelry payments can be useful.

In this article, I’ll outline the highlights you need to know about BNPL jewelry, from making smart choices to choosing the right provider. Let’s get started.

Key Takeaways

- BNPL Adds Flexibility: Buy now, pay later can make jewelry purchases easier to manage by splitting the total into smaller payments.

- Intention Matters: BNPL works best when you’re buying jewelry for a clear reason, not just because the first payment looks low.

- Quality Still Comes First: The payment plan doesn’t matter much if the jewelry itself isn’t worth buying.

- Read The Details: Always check materials, sizing, return policies, shipping timelines, and payment dates before checking out.

- Sezzle Is Worth A Look: If Sezzle is available, it can be a simple BNPL option to consider for rings, necklaces, bracelets, and gifts.

Why BNPL Works Well for Jewelry

Jewelry is different from a random impulse buy.

A good piece can last for years. Some pieces are sentimental. Others become part of your daily style. That makes the payment structure matter less than whether the jewelry is actually worth owning.

BNPL can help when you’ve found the right piece but don’t want to pay the entire cost at once.

For example, maybe you’re choosing between a cheaper plated necklace and a better-quality gold-filled one. The second option may cost more upfront, but it could hold up better over time. Splitting the payments can make that better choice easier to manage.

That’s the best use case.

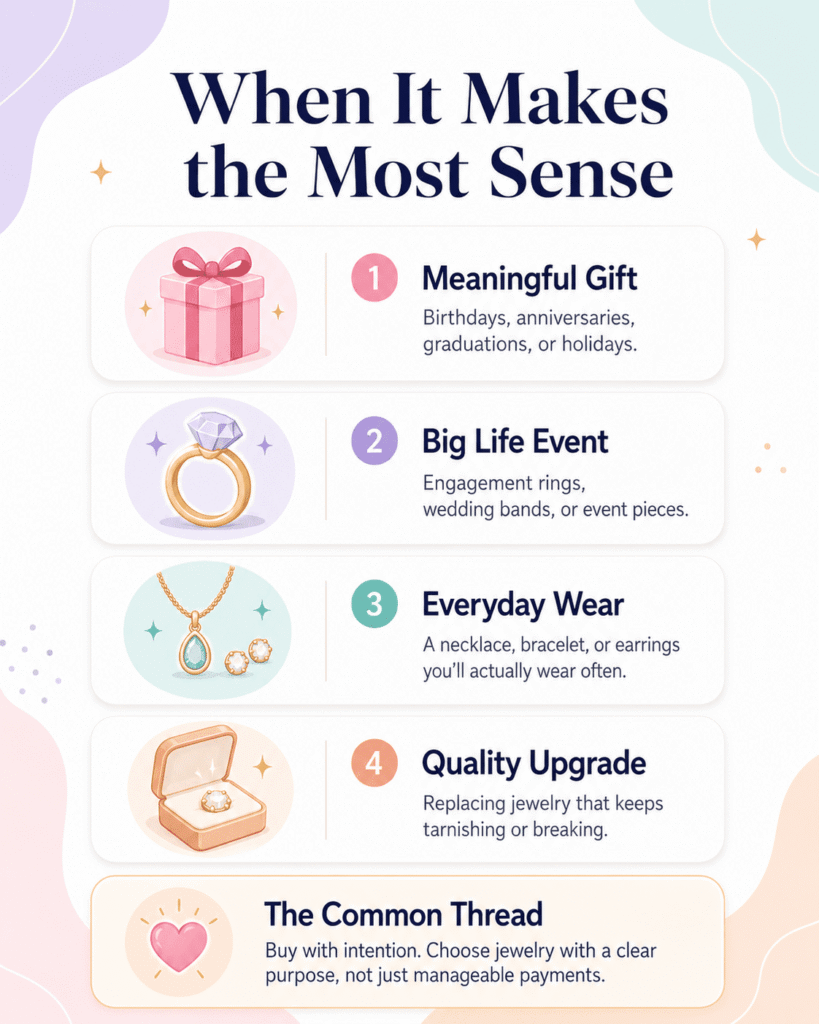

When It Makes the Most Sense

Buy now, pay later jewelry is usually most helpful when the purchase has a real reason behind it.

Good examples include:

- A gift for a birthday, anniversary, graduation, or holiday

- An engagement ring, wedding band, or event-related piece

- An everyday necklace, bracelet, or pair of earrings you’ll wear often

- A quality upgrade from jewelry that keeps tarnishing or breaking

The common thread is intention.

You’re not just adding things to your cart because the payments look manageable. You’re buying something with a clear purpose.

The Part People Get Wrong

The biggest mistake with BNPL is focusing only on the first payment.

A $200 piece may look harmless when the first payment is $50, but it’s still a $200 purchase. That’s not a reason to avoid BNPL; it’s just a reason to be honest with yourself before checking out.

The better question is simple:

Would this still feel like a good purchase if you paid in full today?

If yes, BNPL may be a useful option. If no, the payment plan might be doing too much of the convincing.

Don’t Overcomplicate the Provider

For buy now, pay later jewelry, I recommend Sezzle as a provider worth checking first.

There are other options you may see at checkout, including Affirm, Klarna, Afterpay, Zip, PayPal Pay Later, and other BNPL services. Those can work too, depending on the store and the terms.

But I like Sezzle for jewelry because it has a solid list of retail partners and gives shoppers both online and in-store BNPL options.

Sezzle’s partner network includes options such as:

- Zales

- Kay Jewelers

- Kendra Scott

- Kohl’s

- Nordstrom

- Anthropologie

- JCPenney

And literally, hundreds more.

The important thing is still the same: check the total cost, payment dates, and return policy before you buy. If the payment setup is clear and fits your budget, Sezzle can be a simple way to make the purchase easier to manage.

A Good Rule Before You Buy

Before using BNPL for jewelry, pause for a second and look at the whole purchase.

Not just the first payment.

Not just the photo.

Not just the fact that the piece would look good with one specific outfit you have in mind. Ask whether it fits your style, whether you’ll use it, and whether the full price feels reasonable for what you’re getting. If the answer is yes, BNPL can be a helpful way to spread out the cost.

That’s the version of BNPL that makes sense. It gives you flexibility without making the purchase feel careless.

Final Thoughts

Buy now, pay later jewelry can be a smart option when you’re buying with intention.

It works well for gifts, everyday pieces, milestone jewelry, and quality upgrades you’ve already thought through. Instead of forcing you to pay everything at once, BNPL gives you a little room to manage the cost in a way that may fit your budget better.

The key is to stay honest about the full price.

If the jewelry is worth buying, the payments are manageable, and the terms are clear, BNPL can make the process easier without making it feel like a stretch.

FAQs

It can be a good idea when the purchase is planned, and the payments fit your budget. It’s especially useful for gifts, everyday pieces, and higher-quality jewelry you already intended to buy.

BNPL is best for jewelry you’ll actually use or value long term. That could include engagement rings, wedding bands, everyday necklaces, quality earrings, bracelets, or meaningful gifts.

Usually, BNPL makes more sense for pieces that are worth spreading payments over. If the jewelry is low quality or something you’ll only wear once, it may not be worth financing.

Look at the full price, payment schedule, return policy, material details, sizing information, and whether the item is custom or final sale. Those details matter just as much as the monthly or installment amount.

Sezzle can be a good option if it’s available at checkout and the payment dates work for your budget. It’s straightforward, which makes it useful when you’re already comparing jewelry details like metal type, fit, and returns.