Choosing between BNPL apps can be stressful, with more than 50 established options to pick from.

And choosing between Sezzle vs. Affirm? It’s no different.

Because they both look good on paper, sure. But it’s tough to know what they actually look like in practice, and how they fit into your day-to-day life, until you try them for yourself.

Well, I’ve put in the work for you, using both Sezzle and Affirm on a variety of purchases—everything from school supplies to vacation expenses.

Here’s my honest take on which is better for your budget.

Key Takeaways

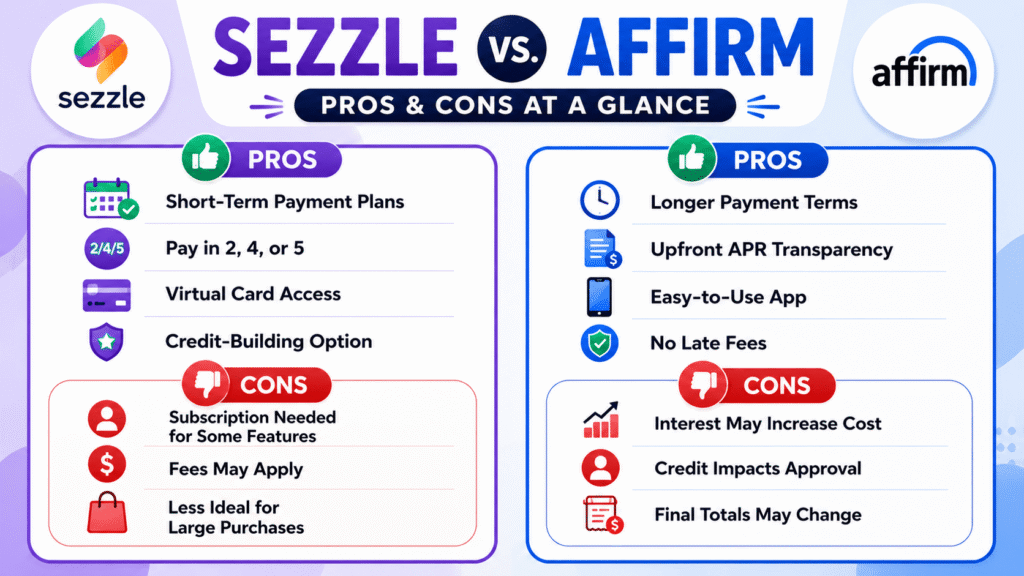

- Sezzle Is Better For Everyday Spending: If you want BNPL for groceries, school shopping, clothes, or household purchases, then Sezzle feels easier to manage.

- Affirm Makes More Sense For Big Purchases: If you’re financing travel, furniture, electronics, or another large expense, then Affirm’s longer monthly plans are more useful.

- Sezzle Feels Easier To Keep Under Control: If you do not want a small purchase following you around for months, then Sezzle’s shorter repayment windows are the better fit.

- Affirm Can Get Expensive Fast: If you choose a longer plan with APR, then Affirm can turn a manageable monthly payment into a much higher total cost.

- Sezzle Has The Stronger Everyday Perks: If credit-building and flexible short-term use matter to you, then Sezzle Up and Sezzle Anywhere make the app feel more practical.

Sezzle vs. Affirm Comparison

| Category | Sezzle | Affirm |

|---|---|---|

| Best For | Everyday purchases, household spending, school shopping, clothes, and short-term budgeting | Furniture, electronics, travel, larger orders, and longer-term monthly payments |

| Payment Options | Pay in 2, Pay in 4, Pay in 5, Pay in Full, virtual card options, and long-term financing options, depending on eligibility | Pay in 4 and monthly installment plans, with available terms shown at checkout |

| Main Strength | Short repayment timelines that are easier to track | Longer repayment options for more expensive purchases |

| Fees + Interest | Pay Later orders at many merchants are interest-free, though service fees and other fees can apply | No late fees, but APR may apply depending on the plan, merchant, and credit profile |

| App Experience | Better for quick payment tracking and everyday control | Polished and easy to use, but more tied to loan-style decisions |

| Special Programs | Sezzle Anywhere, Sezzle Up, Sezzle Spend, and subscription-based virtual card access | Affirm Card, Affirm Money, purchasing power, and monthly financing tools |

Overview: Sezzle and Affirm

Sezzle

Sezzle is a BNPL app that focuses on shorter repayment plans. The most popular option is Pay in 4, which splits your purchase into four payments. Sezzle also offers Pay in 2, Pay in 5, Pay in Full, virtual card access, and long-term financing, depending on your eligibility and what you buy.

Sezzle Anywhere adds another layer by letting eligible U.S. subscribers use a Sezzle virtual card virtually anywhere Visa is accepted, with restrictions. Sezzle also offers Sezzle Up, which can report eligible payment history to credit bureaus after a user opts in.

Pros

✅ Short-Term Payment Control: Sezzle works well when I want to split a purchase without turning it into a months-long obligation.

✅ Several Smaller Plan Options: Sezzle is not limited to Pay in 4, since Pay in 2 and Pay in 5 may also appear depending on the situation.

✅ Virtual Card Access: Sezzle Anywhere can make the app usable beyond a standard checkout button for eligible subscribers.

✅ Credit-Building Angle: Sezzle Up adds a more useful long-term feature by allowing enrolled users to report their payment history.

Cons

❌ Subscription Limits Flexibility: The most useful virtual card access may require a paid Sezzle subscription.

❌ Fees Can Still Show Up: Sezzle can involve service fees, reschedule fees, failed-payment fees, or other costs depending on how the order is handled.

❌ Not Ideal For Major Purchases: Sezzle’s shorter setup is useful for normal spending, but it may not offer enough time for a large expense.

Affirm

Meanwhile, Affirm focuses more heavily on installment financing. It offers Pay in 4 for some purchases, but its bigger distinction is monthly payment plans that can stretch much longer than a standard short-term BNPL schedule.

Affirm displays your available plans and APR options at checkout. It does not charge late fees, prepayment fees, annual fees, or fees to open or close your account. The APR and available plans can change depending on your credit, the store, and what you are buying.

Pros

✅ Longer Repayment Terms: Monthly plans can give shoppers more time than a standard six-week installment schedule.

✅ Upfront Cost Preview: Affirm shows payment options and APR before checkout, which helps make the commitment clearer.

✅ Polished App Flow: The app is easy to move through when browsing stores, checking terms, or reviewing payment options.

✅ No Late Fees: Affirm does not charge late fees, although missed payments can still affect credit and future eligibility.

Cons

❌ Interest Can Change The Value: Affirm can be 0% APR in some cases, but longer plans with APR can make a purchase noticeably more expensive.

❌ Credit Plays A Bigger Role: Better terms depend partly on creditworthiness and other approval factors.

❌ Checkout Totals Can Shift: Taxes, add-ons, upgrades, or final pricing changes can make the plan feel less seamless if the amount changes before checkout is complete.

Payment Options

Sezzle offers the kind of payment flexibility that fits into my everyday life. When I buy things like school supplies, clothes, or household essentials, I do not want a bunch of complicated financing choices. I’m looking for a simple plan that is easy to track in my budget.

That is where Sezzle works so well.

Pay in 4 is the easiest version to follow, and the fact that Pay in 2 or Pay in 5 may also appear gives it some range without making the app feel like a loan marketplace. For everyday purchases, I also like that the repayment structure usually stays close to the original purchase instead of following me around for half a year.

Affirm has the bigger payment range, and that is its best argument. I would not use Affirm casually for a small order, but for travel, furniture, electronics, or a larger one-off purchase, the longer monthly plans can be helpful.

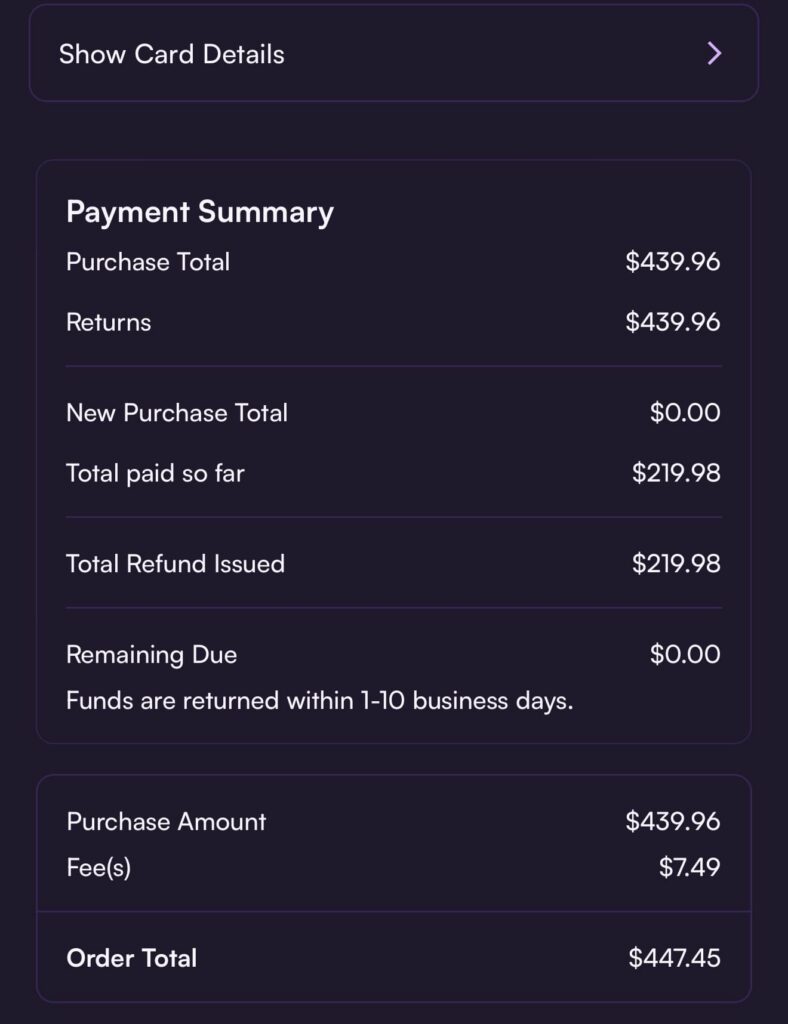

When I booked a vacation, I saw why people like Sezzle. The monthly payment showed up right away, the process was quick, and it made the purchase feel possible almost instantly. Also, if there is an issue like a cancellation, refunds are easy. But this kind of flexibility also changes how you think about spending.

With Affirm, I have to consider if I am okay with owing money for months, not just if the first payment seems affordable now. However, I have used Affim for travel as well, and it has paid off. For example, when Spirit Airlines went bankrupt, they fought for us to get our 4k in tickets back and put the BNPL loan on hold while they worked it out. They even gave us another payment plan to get flights with someone else so we wouldn’t be stranded.

Winner: Affirm. Affirm is stronger on payment options because its monthly plans give larger purchases more room than Sezzle’s shorter repayment setup.

Fees + Interest

I find Sezzle easier to manage because the repayment period is shorter, and I can usually see the costs before I decide to use it. I know Sezzle isn’t always free, as there may be service fees, subscriptions, or other charges. Still, the way it works feels more straightforward to me.

When I used Sezzle for a back-to-school purchase, I could easily see the coupon, the fee, and how the payments would work. That made the decision feel solid. This is what I want from BNPL: some extra flexibility, not a payment plan that becomes complicated.

Affirm is more complicated because it can be very reasonable or very expensive, depending on the terms. I like that Affirm shows the payment schedule and total cost upfront, and that it doesn’t charge late fees.

But the real issue is interest. A 0% APR offer can make sense, while a longer plan with a high APR can make the final cost feel much harder to justify. In the flight example I looked at, an $800 purchase over 12 months at 36% APR would end up around $969 total, which means the convenience of stretching the payment would cost about $169. That is not automatically wrong, but it is too much to ignore. That said, APR and available plans are shown at checkout and can vary by creditworthiness and where someone shops—so, your mileage may vary.

Winner: Sezzle. Sezzle is the better fit for everyday cost control, while Affirm requires more attention to APR and total repayment amount.

User Experience: Mobile App

Sezzle’s app is better suited to how I want to use BNPL most of the time. I’m not opening a payment app because I want to be talked into a bigger purchase; I’m opening it because I want to know what is due, when it is due, and whether I still feel okay about the payment schedule.

Sezzle feels better for quick check-ins. Since the purchase stays close to the payment timeline, it’s easier for me to keep track of what I owe without having to think about it too much.

I do love the shopping aspect of Sezzle. Especially with their “under $100 sections.”

Affirm’s app looks more polished than I thought it would, and I didn’t find it confusing. When I used it for travel, I could browse, check my options, and see the monthly breakdown right away. Getting approved for the Affirm Card also made the app feel easy to use in the moment.

What bothered me was how awkward the app got when the total changed. When taxes and extras made the vacation upgrade more expensive, I had to go back, change the amount, and redo the plan. It wasn’t a big problem, but it showed me that Affirm works best when you know the final price before setting up the payment plan.

Winner: Sezzle. Sezzle is better for simple payment tracking, while Affirm’s app works well but feels more dependent on the purchase details staying stable.

Memberships + Special Programs

Sezzle’s extra features feel more connected to how I would want to use BNPL responsibly. Sezzle Anywhere is useful because it can make the app work in more places through a subscription-based virtual card program, giving eligible users access beyond stores that directly offer Sezzle at checkout.

That added flexibility makes the app feel more practical for everyday spending. Still, Sezzle Up is the feature that matters more to me.

I appreciate that Sezzle lets users link their repayment habits to credit-building if they choose to opt in and qualify. This feature makes the app seem less like just a spending tool and more like something that can help build better financial habits when used thoughtfully.

Affirm’s broader features are useful, but they push the product further into financing territory. The Affirm Card can make installment payments available in more situations, and Affirm Money provides the company with a broader financial ecosystem.

I understand the appeal, especially for someone who already likes Affirm’s monthly payment style. For me, though, those features make Affirm feel more serious, not more casual. That is fine for a large purchase, but it is not the experience I want for ordinary spending.

Winner: Sezzle. Sezzle’s programs feel more useful for everyday budgeting and credit-building, while Affirm’s tools are better suited to bigger financing decisions.

Final Verdict

Sezzle works better for everyday buy-now, pay-later needs. I prefer using it for things I want to pay off quickly, like school supplies, household goods, groceries, clothes, or small emergencies. It gives me enough flexibility to make shopping easier, but it doesn’t push me to turn regular spending into a long-term payment plan.

Overall, Sezzle is better for managing everyday spending, while Affirm is more useful for larger purchases that need longer financing. Affirm offers more payment options, but I trust Sezzle more for sticking to a regular budget.

FAQs

Is Sezzle better than Affirm?

Sezzle is better for everyday purchases and short-term budgeting. Affirm is better for larger purchases that need longer repayment terms.

Is Affirm better than Sezzle for large purchases?

Yes, Affirm is usually stronger for larger purchases because it offers longer monthly financing options. That makes it more useful for things like travel, furniture, and electronics.

Do Sezzle or Affirm charge interest?

Sezzle’s short-term plans are often interest-free, though fees can still apply. Affirm can be interest-free in some cases, but monthly plans may include APR, depending on the offer.

Which app is better for budgeting, Sezzle or Affirm?

Sezzle is better for budgeting because the repayment timeline is shorter and easier to track. Affirm can work well, but longer terms require more attention to the total cost.

Do Sezzle or Affirm help build credit?

Sezzle has a clearer credit-building feature through Sezzle Up for eligible users who opt in. Affirm may report some loans, but its credit impact depends on the product and repayment behavior.